SINGAPORE (ICIS)–Asian butadiene (BD)

producers are turning to the acrylonitrile

butadiene styrene (ABS) market for demand amid

eroded margins and weak buying interest from

main downstream synthetic rubber sector.

“The downstream ABS makers use less BD and can

afford to pay more for BD, so some BD suppliers

will continue to hold out for higher prices due

to the eroded margins,” a trader said.

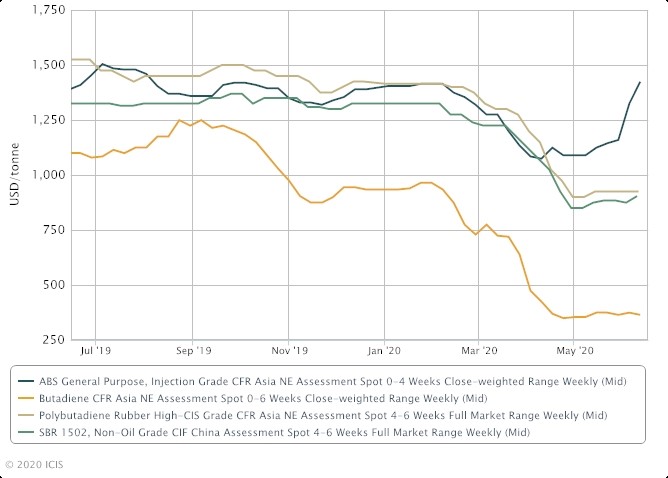

ABS accounts 15-20% of the BD market, while

synthetic rubbers have a much bigger share at

roughly 70%, according to market sources.

Regional BD producers have been unwilling to

offload cargoes at below $400/tonne CFR (cost

and freight) northeast (NE) Asia following

recent spikes in crude and naphtha costs.

But supply in the region is ample and will

further grow given an estimated 150,000 tonnes

of deep-sea cargoes from Europe and the US

arriving in Asia in the second and third

quarters.

This condition dampens spot buying interest

from major consumers in the styrene butadiene

rubber (SBR) and polybutadiene rubber (PBR)

markets, widening the gap between buying and

selling ideas.

On 12 June, spot BD prices were assessed down

$10/tonne week on week at $330-400/tonne CFR NE

Asia, ICIS data showed.

“Naphtha price is similar to BD price, and

regional producers will hold out for at least

$400/tonne CFR basis due to the margins

erosion,” a trader said.

At midday, naphtha prices stood at $341/tonne

CFR Japan, ICIS data showed.

BD must be higher than naphtha by about

$100-150/tonne for BD producers either to break

even or generate margins depending on their

costs structure and sales strategy,

market sources said.

“The market is imperfect, it will eventually

find its equilibrium,” a regional BD producer

said.

Focus article by Helen Yan

Visit the ICIS Coronavirus

topic page for analysis of the impact on

chemical markets and links to latest news.