Sundry Photography/iStock Editorial via Getty Images

Applied Materials (NASDAQ:AMAT) is scheduled to announce FQ3 earnings results on Thursday, August 18th, after market close.

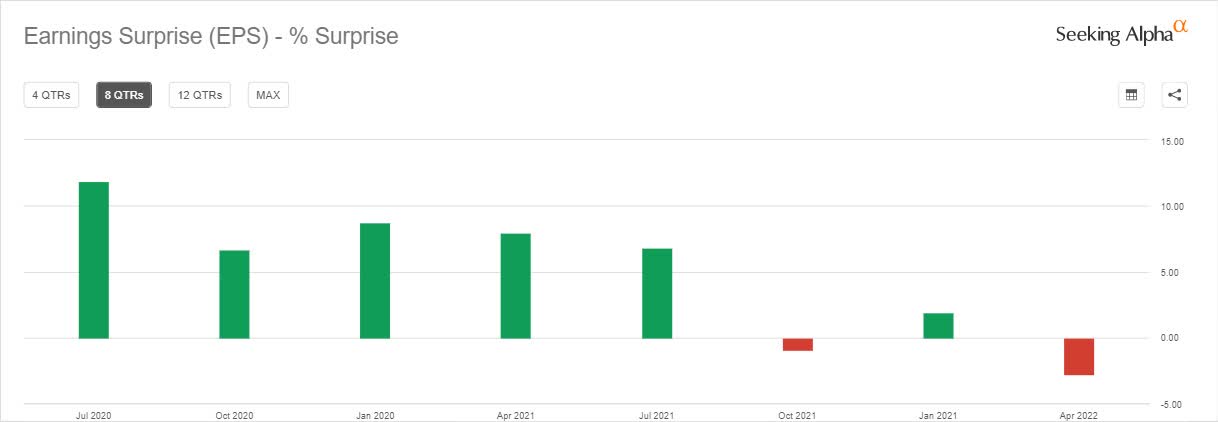

The semiconductor equipment company has beaten EPS estimates 75% of the time over the last two years, but the two misses have happened in the last three quarters.

Applied Materials posted Q2 results that missed estimates and issued weak guidance, leading some Wall Street analysts to cut their price targets. Supply chain constraints have been hurting the company, including in the latest quarter, and investors will be looking to see if this has hurt sales.

The firm will also deal with a $150M impact from COVID-related constraints in Q3, and the wafer fab equipment (WFE) market still appears constrained, although demand is strong.

Morgan Stanley cut 2023 earnings estimates on Applied Materials and peers Lam Research (LRCX) and KLA (KLAC) in late July over worries of cuts to semiconductor equipment spending. Earlier in the month Wells Fargo also cut estimates, noting the current quarter is likely to be a “difficult setup” for semiconductor equipment makers.

Over the last three months, Applied Materials EPS estimates have seen 0 upward and 20 downward revisions. Revenue estimates have seen 1 upward and 16 downward revisions. The consensus EPS estimate is $1.79 (-5.8% Y/Y) and the consensus revenue estimate is $6.27B (+1.1% Y/Y).

Yet Riley Securities has projected an above-consensus performance for Q3. In an analyst note ahead of the earnings, it said although supply chain and shipping issues persist, a robust backlog, new product SAM expansion and powerful underlying services growth drivers will push up sales.

Stifel also expects some improvements heading into H2, with positive spending trends although it believes management will lower 2022 WFE projections. Citi sees H2 equipment sales growth as well as supply catches up with demand, although H1 sales will likely drop on demand fall off, with weak preannouncements by Nvidia (NVDA) and Micron (MU) as lead indicators.