China’s cross-border trains under the Belt and Road Initiative (BRI) have remained resilient and have become a leading option for many international traders, given its competitive advantage, especially as sea transport keeps experiencing congestion and container shortage at many major ports.

The Russia-Ukraine conflict and the COVID-19 resurgence in China have created various unprecedented challenges for cross-border trade. But rail freight service from China to Europe and other countries have been a saviour, protecting from the potential risks of disruption in supply chains. The main benefits include speed and cost as rail freight transport is faster than sea freight, and more cost-effective than air freight.

China-Europe Railway

China-Europe railway routes have become an important means of trade between China and Europe. The China-Europe freight train service is 13,000-kilometre cross-continental transport line linking China and Europe and is playing a strong role in stabilizing the global supply chain while driving their economy towards growth. Russia’s war with Ukraine is regarded as the bottleneck in the growth. To avoid transporting goods via Russia, a new southern route has been opened across the Caspian Sea and the Black Sea allowing entry to Europe via Romania, although capacity on this slower route is limited. However, there has been barely any disruption to the train service even with the heightened geopolitical tensions in Europe.

From 2016 to 2021, the annual number of China-Europe freight trains increased from 1,702 to 15,183, with an average annual growth rate of 55 per cent while the annual value of goods transported rose from $8 billion to $74.9 billion. Moreover, the rail service’s share of total trade between China and Europe rose to 8 per cent in 2021 from 1.5 per cent in 2020, helping their supply chain stability. From January to June 2022 a total of 7,473 freight trains operated between China and Europe, carrying a total of 720,000 TEU. Compared with 2021, these figures were up 2 per cent in number of trains and 2.6 per cent by volume.

The Shanghai Cooperation Organization Local Economic and Trade Cooperation Demonstration Area (SCODA) in the eastern Chinese coastal city of Qingdao saw a much busier China- Europe freight train service in the first half of 2022. The demonstration area handled 430 outbound and inbound China-Europe freight trains in the period, up 44.8 per cent YoY. The inbound trains carried 17,000 containers while the outbound trains sent 18,000 containers in the first six months of 2022.

In July 2022, Fuzhou, the capital of east China’s Fujian Province, launched its first China-Europe 9,900-km-long freight train. The train named ‘Mindu’ departed from Jiangyin Port in Fuzhou with Moscow as its destination. The train was loaded with 455 tonnes of goods valued at $1.8 million. The train is expected to take 16 days to reach its destination, i.e., nearly 20 days less than if they were shipped by sea. During the same month, another new China-Europe freight train departed from Chongqing to reach Melzo in Italy, carrying goods worth $10 million including daily necessities, clothing, household appliances, and machinery equipment. The entire trip is estimated to take about 22 days.

Two more China-Europe freights rail services started in July from Jinhua in East China’s Zhejiang province to reach Venlo in the Netherlands and from the Shijiazhuang International Dry Port in Hebei to reach the BILK intermodal terminal in Budapest, with an estimated transit time of 22 days and 18 days respectively. The service is expected to boost the textile-apparel trade between China and the two European countries.

The China-Netherlands train’s departure marked the launch of the first China-Europe freight train from Zhejiang to the Netherlands as well as the departure of the 400th China-Europe freight train managed by Jinhua in 2022. The China- Hungary train will transit through Mongolia after passing the Erenhot border crossing and then travel via Russia, Belarus, Poland, and the Czech Republic, all the way to Budapest along the main line of the China-Europe train.

China’s Jinhua and Shijiazhuang ports have been busiest since the start of this year. Jinhua had 368 inbound and outbound China-Europe freight trains, which transported 30,368 containers of goods, in the first half of this year, an increase of 8 per cent YoY, while Shijiazhuang operated 186 international trains, an increase of 125 per cent YoY, with transport routes diverging to more than 40 countries and regions such as the European Union, Central Asia, and ASEAN. Additionally, Shijiazhuang port has been following the ‘ Shi Europe’ model, i.e., the model of gathering goods from the surrounding regions and cities in Shijiazhuang and then sending abroad collectively. This has proved to be very efficient since the recently launched Hebei-Hungary service is one of the many running under this concept.

China-Kyrgyzstan-Uzbekistan Railway

After 20 years of negotiations, the construction of the China-Kyrgyzstan- Uzbekistan (CKU) railway is expected to start in 2023. Amidst the Russia-Ukraine crisis, the CKU railway offers several economic prospects for China. Since the war started, businesses have decided to stop shipping goods via Russia. The CKU railway will give China the chance to diversify its trade routes, reduce its dependency on Russian routes, and maintain viable commerce with EU countries in the long term. The CKU will act as a path to the EU via Iran and Turkey, with a total length of 523 km including 213 km in China, 260 km in Kyrgyzstan, and about 50 km in Uzbekistan.

The CKU rail route will not only reduce China’s dependency on Russia but also decrease its dependence on Kazakhstan as a transit country. The recent violent unrest in Kazakhstan showed that reliance on any one country for trade in Central Asia for railway trade may be risky. In this context, the CKU railway can help China diversify its rail routes and switch cargoes from one route to another during future crises. In addition, the new railway will also contribute to Kyrgyzstan’s and Uzbekistan’s economies by reducing the cost of transport and generating employment.

The CKU railway also will generate economic opportunities for China. Through this new route, Beijing will be able to send its goods to both the Middle East and European markets. The CKU railway will be one of the shortest routes to send cargo to both regions as it will shorten the freight journey by 900 km while saving seven or eight days in shipping time. Along with the Middle Corridor, the CKU railway can help increase the cargo capacity of Central Asian countries through East-West trade. It will help improve the overall economic situation in the central and western regions, which can reduce the risk of social instability. In addition, the CKU railway project will revive the ‘Middle Corridor’ potential to Europe, which was earlier considered costly compared to the land route via Russian territory. The other component of the ‘Middle Corridor’ is Baku-Tbilisi-Kars (BTK) railway, which is another route that will heavily rely on Chinese suppliers to ship their cargo to Europe.

China-Asean Railway

China has been trying to raise bilateral trade with the Association of Southeast Asian Nations, or ASEAN, and has been building several railway lines under BRI that would link ASEAN’s railway network by opening wider opportunities for trade. The China- Laos Railway has facilitated the full flow of goods, services, and factors of production at both the domestic and international levels. Since the Regional Comprehensive Economic Partnership (RCEP) agreement took effect in January 2022, the destinations of international freight via the China-Laos Railway have been expanded to more countries and regions, including Thailand, Malaysia, and Cambodia.

The railway has become a convenient logistics channel between China and ASEAN. Through the railway, China has so far imported about 120,000 tons of goods with a value of more than 500 million yuan and exported over 70,000 tons of goods with a value of over 1.7 billion yuan, according to China’s Custom. In the first half of 2022, 379,000 TEUs of cargo have been sent by the land-sea freight trains of the New International Land-Sea Trade Corridor, up 33.4 per cent YoY. The number of trains operating within the sea-rail intermodal service of the New International Land-Sea Trade Corridor had surged from 178 in 2017 to 6,117 in 2021. It has given a big push to railway transport that has previously been underutilised in ASEAN while mending supply chain disruptions.

The China-Laos railway, which opened in December 2021, has been operating successfully for more than six months now. The rail freight line has improved the flow of goods between China and Laos, as well as among members of the ASEAN. The 1,035-kilometre line runs between Kunming, the capital of Southwest China’s Yunnan province, and Laos’ capital Vientiane. The trip takes about 10 hours, with speeds reaching up to 200 km per hour.

In July, a new freight transit yard was developed at the Vientiane South Station on the China-Laos Railway, with the first railway containers heading to Thailand’s Laem Chabang port. This new transit yard reduces lead time by saving one day while delivering goods between China’s Kunming City and Thailand’s Laem Chabang Port, thereby reducing 20 per cent of transport costs. The facility will enable goods along the railway to reach northward to connect the China-Euro railway and southward to the port of Laem Chabang, further boosting trade between China and ASEAN countries. This freight transit yard of the China-Laos Railway is expected to work to improve the efficiency of freight transport between China and ASEAN, providing reliable transport support for the China- Laos Economic Corridor.

The World Bank estimated that the railway could potentially increase aggregate income in the land-locked country by up to 21 per cent over the long term, and Laos’ link to the broader BRI network could increase its GDP by up to 21 per cent as well.1 By 2030, the freight rail is expected to move up to 2.4 million tonnes of freight each year between China and Thailand, Malaysia, and Singapore. Moreover, the total transit trade by rail between China and ASEAN would account for more than half of the region’s railway traffic and reach 3.9 million tonnes of freight by 2030.

The rising trade is often attributed to the implementation of the RCEP, which is also providing a more integrated regional supply chain and has triggered the growth potential of cross-border trains. Moreover, the rising air and ocean freight shipping charges have also been pushing more companies towards rail transport.

The number of cargo cross-border trains between China and Vietnam has tripled since the beginning of 2022. The Pingxiang railway port saw $972 million worth of goods in the first quarter, a 240 per cent YoY increase. China also has launched several new freight routes from Chongqing and Chengdu provinces, empowering Vietnam and ASEAN exporters to establish new trade prospects with Western China. These routes will reduce the transportation time from an average of 20 days to between five and seven days.

Chengdu has also opened a road-rail transport link through Myanmar – and provides trade routes to the Indian Ocean. The route is the most convenient land and sea channel linking Southwest China and the Indian Ocean and provides an alternative to China’s fear of maritime blockage at the Straits of Malacca (a narrow stretch of water, 580 miles in length, between the Malay Peninsula and the Indonesian island of Sumatra).

Chinese customs data showed that trade via train between China and ASEAN expanded 3.5 times in the first quarter of this year. China’s trade with ASEAN totalled over 1.35 trillion yuan in the first quarter of 2022, an increase of 8.4 per cent YoY, as ASEAN continues to be China’s largest trading partner. According to S&P Global, the manufacturing purchasing managers’ index of ASEAN members was 52.0 in June 2022, signalling the solid health of the manufacturing sector with firms experiencing a higher volume of new orders.2

China and Thailand have recently pledged to finish a long-delayed high-speed rail line linking Thailand to China through Laos by 2028. The 609-kilometre railway line from the capital Bangkok to the Lao border at Nong Khai has only been completed 5 per cent till now. Nong Khai is just across the Mekong River from the Lao capital of Vientiane, where a high-speed train to the Laos-China border started service in December 2021. With trains running at a maximum speed of 250 km/h, the new line will reduce the time the Bangkok-Nong Khai journey takes now on existing standard-gauge tracks. This project is part of China’s long-term plans to link its Yunnan province to the ports of Singapore via high-speed trains cutting through Laos, Thailand, and Malaysia.

The Jakarta-Bandung high-speed railway project, with a design speed of 350 km/hr, is a $6 billion railway line that aims to connect the Indonesian capital city to the textile hub of Bandung, reducing travel time from more than three hours to only 40 minutes. China was selected by Indonesia over Japan to build Indonesia’s first fast-train rail link due to China’s superior financial structure. The project is being developed by PT Kereta Cepat Indonesia China (KCIC) (60 per cent) and China Railway International (40 per cent). Although construction began in 2016, there have been extensive delays due to the pandemic. In April 2022, KCIC announced that the project was 82 per cent completed with plans to be operational by June 2023.

Impact On the Textiles And Apparel Industry

China’s textile and clothing sectors have been benefitting quite well from China’s BRI, with its provinces and transport hubs linking to global supply chains and improving the existing ones. China’s rail development under BRI is providing textile and apparel manufacturers with both opportunities and challenges in optimising and restructuring the networks of their production facilities.

In the past 5 years, China’s textiles and apparel exports expanded by 18.68 per cent and reached $305 billion in 2021. China has been the world’s largest producer and exporter of textiles and clothing for a long time with the country being the largest producer of cotton in the world. China’s low labour costs have acted as a catalyst in keeping it at a high position in world trade. Although China has recently started losing its labour cost advantage, it still successfully upholds its leading position in the industry by maintaining its competitive advantage in labour-intensive textile products with the relocation of the textile and apparel manufacturing from China to ASEAN countries and establishing new factories along the Belt and Road. The key objective is to “Collaborate for Success” and provide a situation where everyone can make a profit.

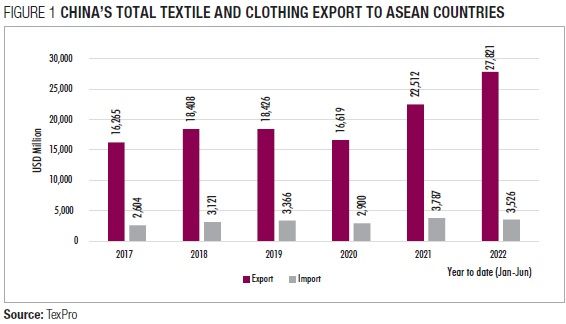

China’s textile makers are more than ready for bigger orders, especially from Southeast Asian nations, since the RCEP deal officially took effect in January 2022. In the first half of 2022, China exported textile and apparel worth some $155 billion, mainly to the US and the ASEAN. According to the data given by China’s Customs, the textiles and apparel exports to ASEAN increased over 23.5 per cent YoY in January-June 2022, and exported $27.82 billion worth of textile and apparel, compared to exports of $22.51 billion during the same period of 2021.

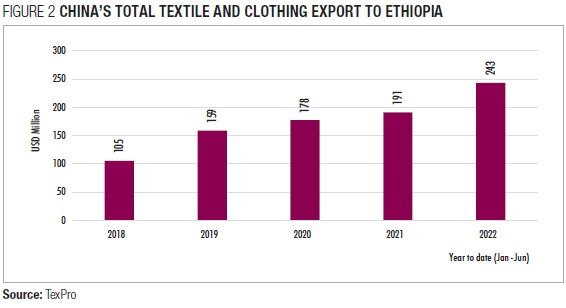

China’s rail freight line is not limited to Europe and ASEAN but has expanded to Africa too. Ethiopia has witnessed the strongest growth through the construction of the Addis Ababa-Djibouti Railway by China under BRI. According to the data given by China’s Customs, the textiles and apparel exports to Ethiopia increased by 27.2 per cent YoY to $243 million in January-June 2022, compared to exports of $191 million during the same period of 2021. Previously, transportation between Ethiopia and Djibouti took more than seven days but now it only takes ten hours to complete the journey. Djibouti is part of the Maritime Silk Road, thereby offering connections to the ports in Guangzhou. In addition, the Mekelle Dry Port, Tigray, which is at the planning stage will improve logistics offerings further on the rail link.

Impact On E-Commerce

Several physical stores closed in 2021 due to the pandemic and people started spending more on e-commerce. In response, retailers have sought to diversify their means of transport due to increased demand and numerous supply chain constraints. China is a significant part of the global e-commerce market due to the manufacturing nature of its economy and the size of the market while European countries are also among the leaders in e-commerce penetration due to their quality characteristics. According to the UNCTAD B2C E-commerce Index, EU countries are the leaders in the number of online buyers. On average, 70 to 80 per cent of internet consumers in the EU make online purchases. Thus, when considering the cross-border online shopping sector, it is trade between China and the EU that is one of the most promising areas for growth.

E-commerce tends towards faster ways of delivering goods, which at the same time are ready to offer a fairly competitive price, i.e., road transport and rail. In the current situation, retailers have found China-Europe freight trains as a cheap and efficient source of freight. Traditionally, e-commerce supply chains relied mostly on maritime or air shipping to transport products in bulk to destination countries where local express providers took final responsibility for the delivery of products to the end customer. From January to May 2022, Chongqing’s cross-border e-commerce imports and exports grew by 88.9 per cent YoY to 19.79 billion yuan. In 2021, Chongqing’s cross-border e-commerce imports and exports reached 32.21 billion yuan, up 63.3 per cent YoY.

This shift is credited to digital advances in e-commerce, which has increased competition among companies, especially in fast fashion. For instance, Shein, one of China’s leading fast-fashion e-commerce retailers, uses customer data to decide on the production of a huge range of trendy apparel at extremely low-price points and in small volumes. These items are then marketed and sold to a particular set of consumers around the globe via online platforms. While its manufacturing base is in China, Shein’s core markets are the United States, Europe, Australia, and the Middle East. In such a scenario, companies find trains as an economical, reliable, and fast mode of transport.

Conclusion

The increasing costs of air and sea cargo shipping have rejuvenated interest in freight rail, which has helped alleviate the global supply chain crisis amid the COVID-19 pandemic. However, due to the focus on road transport for the past decades and consequent under-investment in rail, ASEAN countries would need to exert extra efforts to take advantage of emerging opportunities in rail transport. An efficient combination of modes of transport will keep overall transport costs low, reduce delivery delays, and sustain established logistics standards. Modern railway infrastructure linking global supply chains could open new trade opportunities, create new jobs, and accelerate the overall growth of the economies. However, this would require policymakers to implement restructuring in the business and trade environment and facilitate well-targeted complementary infrastructure investments.