COVERAGE INITIATION: Boxlight (BOXL)

Stock Rating: SELL SHORT

Price Target: $1.04 (+50% upside)

Market Close Price: $2.07 as of 8/7/2020

Boxlight (BOXL) is one of the most speculative stocks

floating high on unsubstantiated rumors that was followed-up with announcements

not tied to revenue growth, but instead a partnership with Samsung, and a

secondary offering for shares which will cause substantial dilution. It’s not

that in all cases secondary offerings cannot be accretive long-term to

shareholders, but without a compelling enough market opportunity, and growth

thesis that can unlock significant ROIC with the use of additional capital… the

stock will flounder.

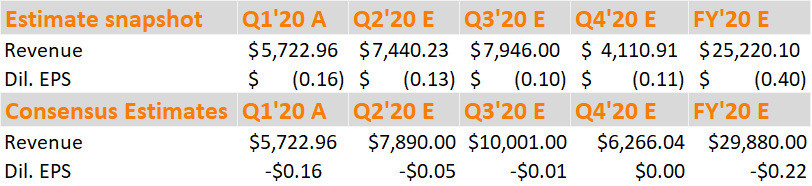

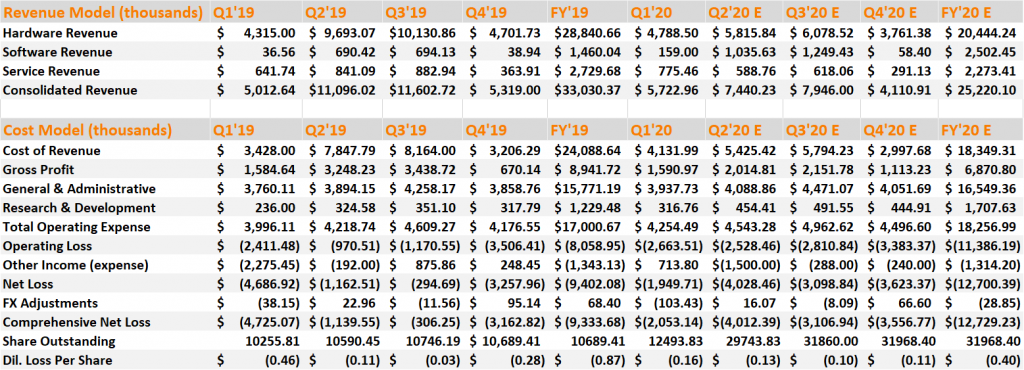

Figure 1. Financial Estimate Snapshot

Source: Cho Research

As such, we assign our $1.04 PT based on a blend of forward

sales multiples in the education space and forecasted tangible book value. In

terms of our Q2’20 estimates, we forecast revenue of $7.44M and dil. Loss of

-$0.13 which compares to consensus at $7.89M revenue and dil. Loss of -$0.05.

Our revenue estimate is $450K below consensus, and dil. Loss estimate is below

consensus by -$.08 as well.

The company recently raised $34.5M addressing immediate

solvency risk as of July 17th, 2020. We anticipate that given the

current cash burn rate, and softening environment, along with the terms of the

agreement outlined by the lead bookrunning agent, i.e. Maxim Group at terms of

$2.00 per share, the stock is hovering dangerously close to the most recent

secondary raise, and prompts the question of an early exit from institutions who

participated in the recent transaction, as most underwriters take a position

and sell out of positions following a cap raise.

In this case, we anticipate that buyers at the secondary

offering will feel pressure in the coming weeks, whereas the agent’s 2.25M

option has been exercised at favorable terms to Maxim Group, which prompts the

likelihood that the stock was propped up temporarily to protect a certain class

of investors while leaving retail investors to hold the bag.

If you were hoodwinked into this stock and find yourself

frustrated with the recent stock performance, we assure you that things could

turn even worse given the context of events leading up to the recent run-up in

the stock, and the material divergence in pricing from the underlying business

thesis in the company. As such, we are hoping that readers will heed our words

of caution, and more adventurous investors follow our logical reasoning tied to

our short thesis on Boxlight.

Bullet Points to our Thesis:

- Boxlight anticipates that they can continue to

raise capital via follow-on offerings as indicated by their intent to raise

$150M when the company’s market cap was $110M. - Business fundamentals do not support a return to

profitability in the near-term much less in the next three-years. Absent of

additional follow-on raises, the company would run out of money and in turn go

out of business. - Willingness of investors to absorb near-term

dilutive impact from additional cap raises seems unlikely as the stock’s total

float barely supports the present valuation and is set to spiral lower based on

weakening sentiment and anticipated dilutive impact from additional secondary

raises. - Absent of near-term business wins tied to

expansion of classroom/school penetration, the business fundamentals will not

be supportive of a secondary cap raise at favorable terms. We anticipate that

by the time the company raises additional capital the stock will trade

meaningfully lower thus diminishing the perceived positive balance sheet impact,

thus continuing the concerns tied to liquidity/solvency. The absence of

retained equity, or minimum stock price could then prompt the notice of a delisting

from Nasdaq due to not meeting listing requirements. - We anticipate that efforts to transition into a

digital classroom came too late in an environment where more established competitors

have built larger business models around content, hardware, learning management

systems, cloud, and integration services. - The absence of meaningful business wins, and a

challenging environment for school re-openings in the United States will

further hinder the fundamental thesis. We anticipate that physical product sales

to schools will perform considerably worse in this environment as alluded to recent

quarterly earnings reports from other providers of supplies/technology products

to K-12 education. - Federal K-12 funding might not fully address the

shortfalls in funding for K-12 education as indicated by the aggregated cost of

schools in the United States, and the state level funding shortfalls due to weakening

budgets at the state level due to lower levels of tax receipts given the

weakness in the current business environment, i.e. COVID-19 recession. - In the upcoming school year, a significant

number of school districts have transitioned to a pure digital environment, and

BOXL’s non-competitive products/services in a pure digital transition when

compared to peers in the segment will translate poorly. There’s not enough time

to implement an untested product in this environment, and we anticipate that

while the transition to digital education in K-12 will provide opportunity for

some companies, we anticipate that it’s also a harbinger of doom for companies

who are mostly reliant on physical product sales to k-12 schools. - This stock will continue to burn capital and the

recent wave of hype and buying on rumors/speculation has driven a wedge between

what investors should believe, and what is likely to occur. When expectations

realign with the impending reality facing laggards in the K-12 space, we

anticipate that investors will experience significant losses.

Why is this secondary capital raise so abnormal?

The size and scope of the offering is abnormal in relation

to a number of factors that have been documented in a study Jonathan Clarke,

Craig Dunbar, and Kathleen Kahle. The study is titled: The Long Run Performance

of Secondary Issues: A Test of the Windows of Opportunity Hypothesis.

More specifically, the rated firm characteristics puts

Boxlight way into the zone of outlier as the firms market-to-book ratio,

offering size, secondary shares/shares outstanding, secondary shares/average

daily trading volume puts the stock in “outlier” territory, but certainly not

in a good way.

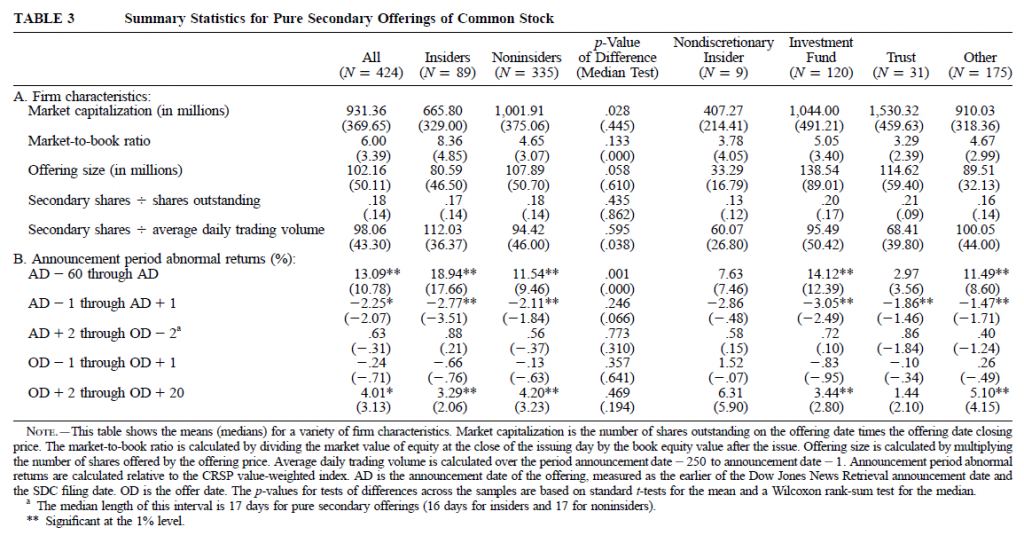

Figure 2. Historical Summary of Secondary Offerings of Common

Stock

Source: Chicago Journals

Based on the weighted average metrics for 424 companies

studied in the above table, the average market cap was $931M, market-to-book

ratio was 6.0, offering size was $102.16M, secondary shares as a proportion of

shares outstanding was .18 (meaning additional shares were 18% of the total

outstanding shares), and the secondary shares would require 98 days of average

traded volume to turnover or equivalent to the number of days based on

historical volume to fully liquidate shares in a normal market environment.

In the figure below we compare the average weighted metrics

of the study, to the proposed offering by Boxlight, and come away with the

conclusion that the offering is a statistical outlier in the worst way

possible, and that the impact it would have on the valuation of the company

goes far beyond what conventional regression, statistical smoothing methods

would be able to capture. However, we anticipate that markets will hinge their

expectations on the historical performance of the company itself, and that

“anchoring” of expectations will lead to the obvious conclusion that they’re

planning on raising money to burn the cash on operations with very low

prospects of ever becoming profitable.

Figure 3. Just how much of a statistical outlier is

Boxlight?

Source: Cho Research

When based on the empirical data we have available on these

types of secondary offerings, generally they tend to have a neutral or not so

significant impact on a company, unless if the impact of the offering is

contingent on funding continuing operations. Notwithstanding, the study on

secondary issues does not suggest that secondary offerings are necessarily bad

for shareholders in general, which is why we tend to maintain our ratings on

equities following cap raises depending on the circumstances and the underlying

drivers of the business.

In this case, Boxlight is an aberration from the mean in a

number of ways. For example, the company’s market to book ratio is lower than

the peer set, mainly because the company is trading at a negative tangible book

value per share, so we default to the 0 “value” (based on the latest financial

filings) and excluding the impact of the $30M recent capital raise. We also

highlight that the amount raised in the offering is equivalent to the mean,

except the average market cap is 1/10th of the peer set average.

This means that in relation to the amount of capital raised in relation to the

underlying market value of the company, they are attempting to raise 10x

more cash. In other words we think the underlying probability of success is

low, as there are very few buyside/institutions that would subscribe to the

secondary knowing how atrociously overvalued the company is, and also knowing

how badly the company needs the cash.

We also examine the presumed share outstanding ratio in

relation to the total number of shares likely issued at the current market

price (which at the time of writing is $2.07). We have seen cases where

secondary issuances are priced above the prevailing and below the prevailing

market price, so we are anchoring our datapoint on the day’s market price for

simplicity.

That being the case, as a ratio of new share issuance, the

company would be issuing 1.61x more additional shares than the total share outstanding

based on the recent filing, and the prevailing market price. What’s more

alarming is that on average companies tend to dilute shareholders by an

additional +18% relative to total share outstanding, but in this case, the

company intends to raise multiple rounds of cash for a cumulative dilutive

impact of +161% up until the stock trades below a market capitalization of

$75 million by which the company would sell 1/3rd the company’s

valued float in any 12-month rolling period following the initial sale of stock,

according to the S-3

filing. This implies that the company is willing to dilute shareholders by 9x

more than the average secondary issuance amount.

What is also worth mentioning in the stats is the number of

days turnover, or basically if volume remains at the current average, the

amount of days it would take to sell the new issuance of shares. This is where

things get a little more alarming. On one hand, the current 365 day average of

volume is 4.07m shares traded, however this figure is a bit inflated, as much

of the volume is concentrated in the one month period of June-July where

average volume was 35.37M, which is 111% of the total share outstanding. The

volume is even more concentrated into a number of day where 318.29M shares

traded on 7/16/20, and 115M shares traded on 7/14/20. When taking into

consideration the price chart (below) we think volume will return to a range of

8K-150K share volume traded per day, which means the stock is presenting an opportunity

to sell short on diminished trading volume, as interest in the stock will

eventually wane on the basis of weak fundamental support, and exhaustion from

bulls that have taken the stock to its 1-year high.

Figure 4. So how do we know volume is arbitrarily

inflated for a short period of time?

Source: Yahoo Finance

We’re more exhaustive than this with our assertion, as U.S.

Equities turnover ratio on an annualized basis is 133%. Meaning that total

traded volume over the course of a year is 133% in relation to aggregated market

cap for all stocks in the U.S. We then divide the annualized figure of turnover

by 365 days to arrive at an average shares traded in relation to total market

cap which is 0.36%. Basically 1/3rd of 1% of total shares are typically

traded in relation to market cap on an aggregated basis across all stocks in

the United States in a given day. Therefore, if volume were to return to more

normal levels, BOXL’s daily volume would return to 115K shares traded per day,

which is why the stats are so distorted when comparing the annual average of

shares traded in relation to secondary issuances.

In most cases, when companies go and raise capital in a

secondary offering the available volume or float is much lower, which is why

company’s typically take into consideration the amount of turnover it would

take to absorb the more dilutive stock based on more normalized volume metrics,

which yields around an average of 100 days.

However, if we were to input the more normalized volume

stats of 115k shares traded per day using U.S. market average for BOXL in

relation to the $150M cap raise, and use the $2.07 price (as of the time of

writing), it would take 690 days for share turnover to be equivalent to the

total new issuance of stock, which is 7x higher than the statistical average

of 98 days for secondary issuances based on the study published by Jonathan

Clarke, Craig Dunbar, and Kathleen Kahle.

I.E., this capital raise will be so dilutive that it is

almost impossible to imagine how this will be good for shareholders. Not to

mention, in the prior price chart, daily trading volume is consistently trending

lower, and so the stock’s price is also trending lower with it.

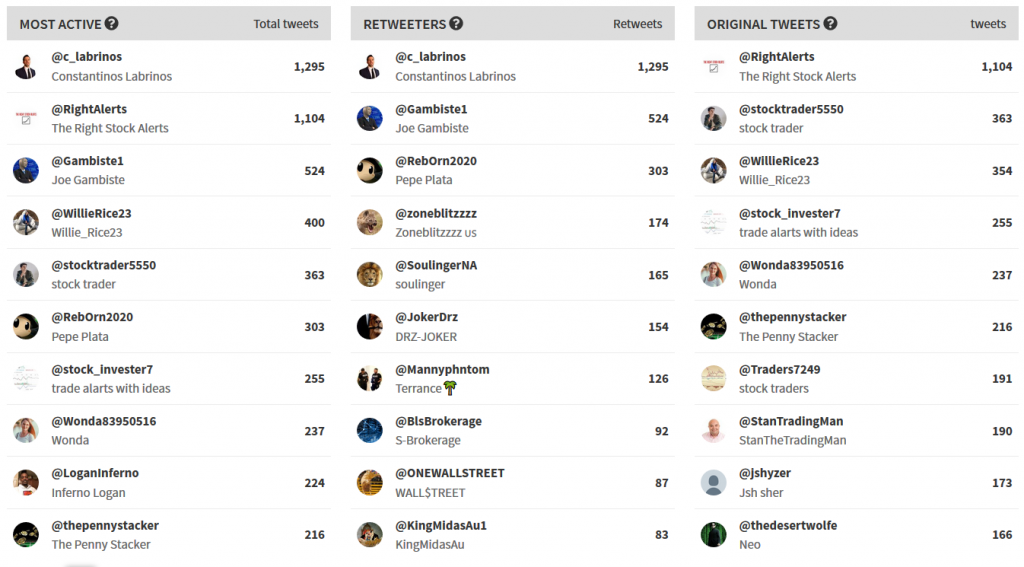

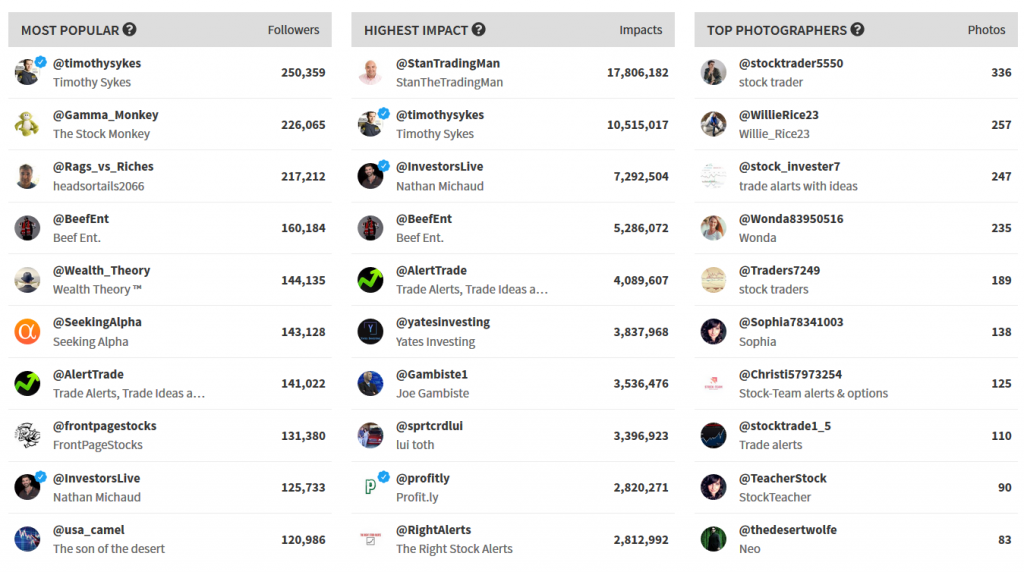

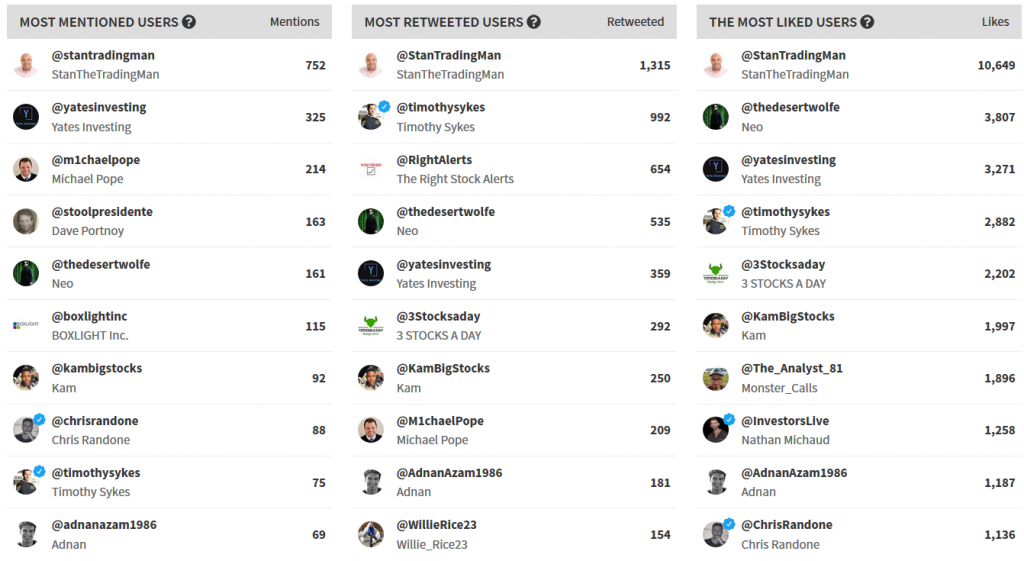

But… what is the source of excitement for BOXL?

Based on aggregated data we were able to compile on the cash

tag $BOXL on Twitter we find that the stock tickers sentiment tracker on

third-party analytics site Tweet Binder to be somewhat alarming. Not only was

the stock heavily promoted by known promoters who do the proverbial “pump and dump”

tripe that is common in the penny stock space, but it got a lot of retail investors

involved. The peak in the stock price formation closely corresponds to the peak

in social media activity. This is defined in the sentiment tracker report we

compiled below, which shows the “biggest promoters” and the volume of tweets and

activity pertaining to Boxlight.

Figure 5. Twitter Activity Tracker

Source: Tweet Binder

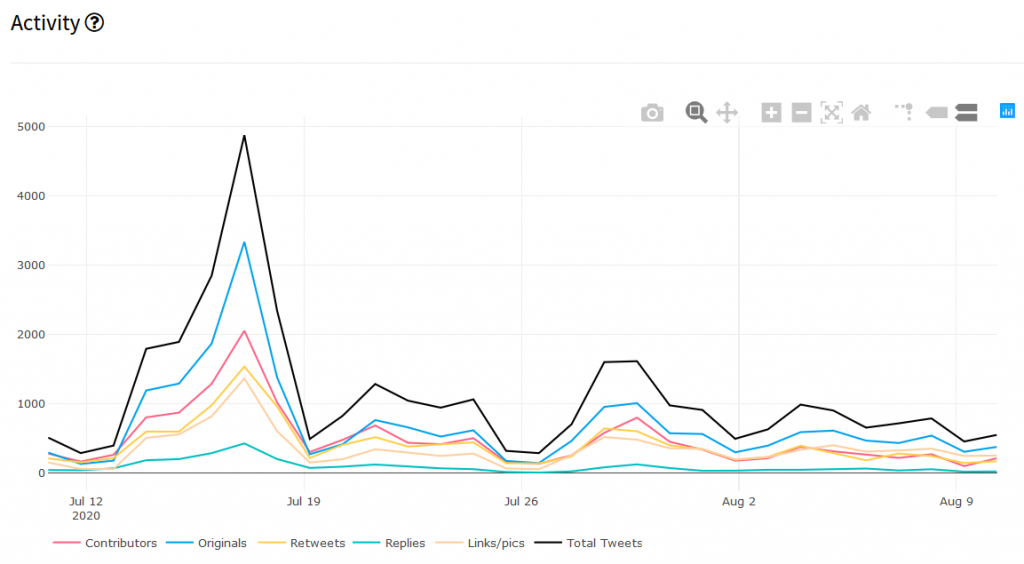

We analyzed data of tweets using the $BOXL tag, and found that the amount of social activity associated with the stock was astronomical leading to its big run. However, when looking at the next graph below, we also identified that the sentiment has trended lower with a small uptick leading to the quarterly earnings report.

Figure 6. Twitter Sentiment Tracker

Source: Tweet Binder

We believe that the sentiment started trending lower between July 10th to July 15th, and we don’t anticipate social activity to return to those levels again for quite a while. Not to mention, the scope of activity suggests significant promotional activity from known “promoters” of smaller cap stocks in hopes of making a quick buck off of less sophisticated investors.

Figure 7. Biggest Twitter Promoters on $BOXL

Source: Tweet Binder

The most recognized promoters were StanTheTradingMan, Timothy Sykes, Gamma Monkey, among many others. We would be be very cautious of this stock, because more often than not they’re promoting on price action, and it has very little to do with underlying business fundamentals aside from rumored events that have already been priced in.

Boxlight’s Business Fundamentals Extremely Weak

The specific areas where sellers into k-12 systems are

experiencing challenges is in physical products. According to a survey from

Education Week over 50% of school district have announced that they will be

going back-to-school in strictly an online only or hybrid environment. Even

with the announcement of the Samsung partnership for online courses, and the existence

of BOXL’s Mimio product we anticipate that the drop in hardware revenue will

mitigate any near-term impact from these new growth initiatives.

Basically, BOXL came to market with a product that it needed

to market since the beginning of last year to gain any meaningful foothold in

the market. Not to mention, there’s steep competition in the segment with

industry stalwarts in LMS (learning management systems) i.e. Blackboard (which

has the highest penetration of users), and digital textbooks/coursework offered

by more established publishers like McGraw-Hill. We anticipate that given the

cadence of the COVID-19 disaster that K-12 Districts will favor established

products in various e-learning environments thus diminishing the bullish case

scenario for shareholders considerably.

If this were a case where BOXL had steadily gained a

foothold in digital/online education from its very inception as a company, the

short thesis would not make much sense in an environment where a majority of

school districts are transitioning to an online environment. However, this is

not the case, as its more akin to a company putting a band-aid on a gushing wound.

We anticipate that once schools make this transition to e-learning that K-12 Education

will turn into a hybrid environment to leverage the new investments into e-learning.

Meaning that budgets that would have been dedicated to hardware in the 21’-22’

school year would be put more towards e-learning, and that a number of efforts

will be made to diminish the use of physical school campuses in general to

balance school budgets.

This transition will mark an inflection point in K-12

education. Therefore, the following year will not necessitate a need for

significant hardware investments but a continuation of on-going software

subscriptions or per user license models for a number of providers that provide

unique services and products to K-12 schools. As such, we think selling of any

form of physical products will enter a period of secular decline and the

emergence of winners in the space is contingent on the degree to which they had

already transitioned revenue mix into digital products/services leading into

the COVID-19 crisis.

Figure 8. Financial Model Overview

Source: Cho Research

Given the high dependency on hardware revenue we anticipate

a material drop in revenues from this category, as we anticipate a 40% decline

in hardware revenue in both Q2’20 and Q3’20 (seasonally strong quarters). We anticipate

that pre-existing school systems that it had contracted with would attach to

some of there new software products, which is why we forecast 50% growth in the

segment, which is quite generous given the poor timing of its recent launch

with Samsung, and the lack of detail tied to its Samsung partnership agreement when

it pertains to revenue share.

Furthermore, the service revenue is mostly associated with

hardware installations, and so we anticipate a similar drop in services as well.

Therefore, we estimate that Q2’20 revenue will come in at $7.44M, which

is below the analyst consensus estimate of $7.89M revenue for the quarter. We felt

that we were generous with our assumptions when making our model, but opinions

may differ especially when BOXL is expected to report earnings on August 11th,

2020 (after the close).

We also anticipate that given the recent raise of $30M at an

average share price of $2.00 that the company is anticipating a significant cash

burn phase. As such, our dil. EPS estimates are lower than the consensus estimate

for both the current quarter and fiscal year. This is driven by heightened

expenses for marketing/selling into K-12 systems new products/services and heightened

R&D spend. We also anticipate abnormalities in terms of “other expenses”

which is mostly driven by underwriting related expenses for the recent $30M cap

raise, which we anticipate a one-time impact.

When taking this into consideration we estimate that the

company will report a dil. EPS loss of -$0.13, which compares to consensus

dil. EPS loss of -$0.11. We anticipate that comprehensive net loss will

increase by 300% from -1.1M to -4M from prior-year. The diminished impact on dil.

EPS is driven by the significant uptick in dilutive impact due to total share outstanding

increasing by 3x versus prior year.

Though our estimate does conform within the consensus range,

there is a decent likelihood that BOXL will burn more cash than what our

estimate implies given the $30M raise, and what’s implied in our model is a

cash burn rate of $7M-$9M for FY’20. We also anticipate that the stepped-up

effort into e-learning will require significant investments, so we are expecting

the company to deliver a significant expense miss in the upcoming quarters.

We arrive at a Price Target of $1.04 (or simply

speaking $1) by basing the valuation on its forward P/S ratio and the

anticipate tangible book value of the firm. More specifically we value the firm

as an average of what its tangibles are worth with the inclusion of its most

recent cap raise (providing the floor to its valuation) and anticipated cash burn/write-offs,

and where education services peers as a sector trade at an average P/S ratio of

1.97x.

Management Discussion

We have

concerns with the current CEO, Michael Pope who was promoted to CEO as

of March 20th, 2020. Prior to running Boxlight he was the Managing

Director of Vert Capital from 2011-2016.

From what we heard from various reliable sources, Vert Capital

had a terrible reputation in the space, as he conducted various “Private Equity”

transactions.

According to the Crunchbase Profile

on Vert Capital, the firm invested into 5 different early-stage ventures, all

of which “busted” and couldn’t proceed to future rounds. The start-ups the

company invested in were Logical Choice Technologies, Hotel Reservations, BigDoor,

PixelMags and Scriba Stylus.

But, beyond the alarm signs associated with his early-stage

investments was the fact that he raised “over $500M” according to his profile

for over 50 control based “transactions.” Its stated in his LinkedIn profile

that he conducted over 40 of those transactions. What’s alarming is the fact

that Vert Capital quickly ran out of capital and could not raise more money

from additional limited partners due (most likely) to the poor performance of

the fund. Hence, Vert capital is no longer active and had to start winding down

their PE fund in 2016.

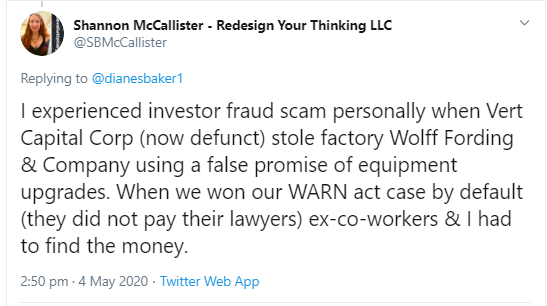

Source: Twitter

We also uncovered some troubling tweets from the past, which

involved Wolff Fording & Company, where the lawyers who won the case

against Vert Capital couldn’t recoup the legal costs associated with the lawsuit

(where the plaintiff recoups legal fees & costs from the defendant). As

such, the troubling past implies that Michael Pope is A) capable of

raising and wasting a lot of investor capital B) will definitely leave

investors footing the bill when things go wrong C) certainly capable of

destroying mid-market firms as opposed to helping them D) Vert Capital couldn’t

manage the “wind down phase” properly and didn’t even have the money to cover

legal fees on behalf of a plaintiff they lost a case to.

Boxlight is by definition a mid-market firm, and after

reviewing his track-record there’s certainly a high likelihood that Michael

Pope will continue to dilute shareholders as indicated by the shelf filing for

$150M and destroy shareholder value in the process. In other words, the new CEO

has a very troubling past and has failed to demonstrate that he can in fact

turnaround companies on a regular enough basis to generate investor returns

where buyouts in the mid-market space are supposed to generated unlevered

returns of 30%+. Instead, he winded down a fund that raised over $500M and

managed to maneuver himself into a management position in a Public Company

where failure is highly visible and difficult to downplay awful quarters much

less hide material financial information.

As such, we think the underlying narrative is quite simple,

if you’re a shareholder of Boxlight its better to head for the exits than leave

money in the hands of a person who can’t manage to generate returns from

mid-market transactions after a sample size exceeding 50 transactions. Sure, he

may have had some successes, but its like betting on a batter with a horrible

batting average, or a reliever pitcher for an awful baseball franchise.

Source: Twitter

The public markets are a much more difficult environment,

and there’s truly little room to hide skeletons in the closet. Much less the

amount of patience afforded to public companies is much shorter than private

companies. So, if the CEO can’t produce results when the spotlight is

non-existent how could he possibly buck the trend in an environment as difficult

as this, especially for K-12 schools?

Final thoughts

We continue to emphasize the troubling pattern of dilution, accumulated

shareholder losses, and the difficult business environment when pertaining to

BOXL. We think there is a compelling short thesis, as the company is nowhere

near generating material software revenue, and we don’t anticipate their

product suite to be as competitive in an environment where K-12 districts are already

struggling with budget shortfalls.

We anticipate that the impending quarterly report will be an

utter disaster for shareholders who have anticipated significant gains in a

stock that cannot back this euphoria with solid business results. Not to mention,

we have concerns tied to the quality of management and particularly the CEO of

Boxlight.

Based on the scope of downside tied to the stock, we anticipate that it will trade at $1.00 creating a compelling a short opportunity. Hence, we assign BOXL at SELL SHORT.

Disclosure: Cho Research was not compensated by Boxlight to publish “Boxlight (BOXL) Set to Crash Post Earnings Setting Price Target at $1.00” Though Cho Research does use the research dollars it generates from other clients of our research service to fund market research

reports such as this. Cho Research may at its sole discretion enter into a short position following the publication of this report. This document is not produced in conjunction with a

security offering and is not an offering to purchase securities. This report

does not consider individual circumstances and does not take into consideration

individual investor preferences. Recipients of this report should consult

professionals around their personal situation, including taxation. Statements

within this report may constitute forward-looking statements, these statements

involve many risk factors and general uncertainties around the business,

industry, and macroeconomic environment. Investors need to be aware of the high

degree of risk in micro capitalization equities, cryptocurrencies, crypto assets.

Independent equity research isn’t regulated by the SEC and operates separately from more conventional sell-side equity research. The publication of independent equity research is unregulated and rules pertaining to published independent equity research are covered under “freedom of the press” with legal case precedent taken all the way to the N.Y. Supreme Court to guard against libel based claims or claims of loss relating to the publication of a report on a company. Any copyright claim relating to infringement is covered under fair use of copyrighted materials. Since the use of material was derived into a separate form of analysis without any substantial content derived from any third-party no copyright claim can be pursued under common law. To discuss investment risk or to consider the risks pertaining to any securities it is recommended to consult a registered financial advisor. To understand independent research it’s encouraged to read this published article on independent equity research to become more familiar with industry standard practices and the relative value of independent equity research versus brokerage research and news media.Cho Research, its subsidiaries, and employees may open along/short equity position at future date from the data of publication of the report. The price per share and trading volume of subject company and companies referenced in this report may fluctuate and Cho Research is not liable for these inherent market fluctuations. The past performance of this investment is not indicative of the future performance, no returns are guaranteed, and a loss of capital may occur. Certain transactions, such as those involving futures,options, and other derivatives, can result in substantial risk and are not suitable for all investors.