Macroeconomic divination

Our purpose and point in studying these various macroeconomic indicators are to try and divine when something is going to change. When’s inflation going to turn up so that the Federal Reserve then changes interest rates? Is there a recession a’comin’? Is there some bubble in the economy that’s likely to burst?

That last concerns us, of course, because the last downturn was caused by just that. However, the more normal cause of a recession is the Fed raising interest rates to head off – or kill off – inflation. So, we should rationally be reading the runes to see whether that’s about to occur.

The answer at present is, well, not as far as anyone can see. The US economy seems to be rumbling along rather nicely. Growth is at about potential, that 2.1% or so annual rate. We’re not seeing any rising inflation, indeed it’s currently a little below target. The one thing we do worry about is, well, where are all the problems? Surely, this can’t just keep going?

Well, there’s no theoretical reason why an economy shouldn’t just continue growing at potential – that’s rather what the definition itself means, that this can just continue.

So, what we’re looking for in this evidence base we’ve got available to us is proof that this isn’t true. That there is some problem building up which is going to bring the current good times to a close. This is why we keep looking, of course, even if there seems to be no evidence of such an event being about to happen.

The latest set of numbers is the JOLTs report. This is the details of hirings, firings, quits, and so on in the labor market. Plus, how many empty jobs there are out there as compared to how many unemployed and so on. There’s no evidence of any change either. In fact, the likely result of these latest numbers is that the expansion is going to last longer than we previously thought it would.

JOLTs

The report itself is here.

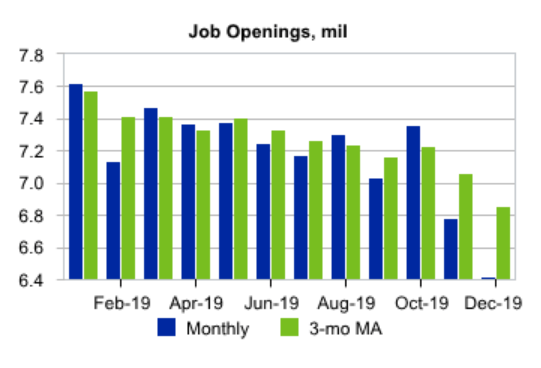

The number of job openings fell to 6.4 million (-364,000) on the last business day of December, the U.S. Bureau of Labor Statistics reported today. Over the month, hires and separations were little changed at 5.9 million and 5.7 million, respectively. Within separations, the quits rate and layoffs and discharges rate were unchanged at 2.3 percent and 1.2 percent respectively.

So, the number of jobs open fell a little. That number is very much larger than the number of people unemployed (which is a guide to but not exactly the same as, the number of people looking for a job). No, it isn’t as simple as everyone getting a job if they want one, there’s the matching process to go through. That’s why we have this idea of “frictional unemployment” and also “full employment” which isn’t unemployment at 0%.

Quits rate

The quits rate is a useful proxy for the upward pressure on wage rates. It was actually Karl Marx who pointed out that once unemployment is effectively conquered, people can only expand the labor they employ by tempting them away from other employers. That means increasing wages (or benefits, or lowering hours, all largely the same thing). Substantial increases in wages will lead to wage inflation and thus the Fed calling an end to the party.

So, a jump in the quits rate, as people do move jobs for those better offers, makes us worry. Yet, that jump isn’t there, so we don’t have to worry.

Layoffs

There are always going to be some layoffs in a market economy, that’s just the way they work. Some companies shrink or fail as others grow. But a sudden jump in that rate would mean that the recession is already upon us. This also, obviously enough, isn’t happening as yet.

Job openings

That there are more jobs available than there are people looking tells us the market is tight, yes. But a tight market isn’t a problem, it’s one that’s “too tight” which is. The definition of “too” there is arguable, but really, it’s one which produces that wage inflation. A bit circular there, but that’s what it means.

Source: Job openings, JOLTs report from Moody’s Analytics

That fall in openings tells us that the market is becoming a little less tight – so no rise in inflationary pressures there. We’re also quite obviously not on the verge of a recession as there are still more jobs than people looking for one.

The Moody’s Analytics verdict looks fair enough to me:

Moody’s Analytics expects the labor market expansion to endure in 2020, but the pace of expansion will slow. We have changed our outlook in recent months. We no longer expect a downturn in the labor market in the second half of the year.

That is, our medium-term outlook for the economy is no change, steady as she goes and so on. There just doesn’t seem to be a macroeconomic problem out there to change things. Sure, of course, events might intervene – political risk leading into the election, coronavirus, things outside the current system could intervene. But from within the workings of the economy, we can’t see any problems.

In more detail

I mentioned this a few days ago. OK, so, we’re worried about a very, or “too” tight, labor market spilling over into causing inflation. That means the Fed raises interest rates, induces a recession, to get rid of the inflation. We’re looking for signs this might happen.

One way it could is that there simply is no more labor to hire. Business wants more people but they’re just not out there. This is something mostly put to rest by that last set of unemployment numbers. We’re still seeing people coming from outside the labour market into it. The unemployment rate is ambling about at generational lows, but real wages are rising only gradually even as we have those large numbers of unfilled jobs. What’s happening is that the employment to population ratio is rising – people who haven’t even been looking for a job are coming into the labor market that is.

This is good. That employment to population ratio is low by US historical standards and low by the standards of some other countries (a full 10 percentage points of the population behind that of the UK, for example). We would think that there’s room for it to rise. That it is rising also means that there’s less pressure on wages – thus inflation – from the low unemployment rate.

What this, in turn, means is that we’re pretty much back where we started. We can’t see anything that is likely to derail this slow but steady expansion. We’ve not got rising inflation. We have growth at potential – by definition, the level we think can be supported long term. We don’t seem to be running out of employable labor as people from entirely outside the market continue to enter.

It’s almost annoying that there’s nothing more exciting to report. Crisis is, after all, interesting, while boring is, well, boring. But as far as macroeconomics goes, boring is also good.

My view

Here, we are in the longest peacetime expansion on record and we can’t really see any end to it. Intellectually, we know that it will end (for all things do, we’ve not beaten the business cycle after all). But there’s just nothing here – that we can see at least, internally to the economy – which is going to be the trigger for that ending.

Our useful conclusion is, therefore, that the expansion is going to continue.

The investor view

We can look at this in two different ways. Well, three. That third is that it will be influenced from outside the economy that brings matters to an end if anything does soon. The pandemic, the election, something outside the normal workings of the macroeconomy.

The other two are a guide but in different ways. One is to say that things aren’t going to change, so we can and should just carry on as we are. The other is the inverse of that – we face no known risks. One implies that we position ourselves for gentle and continued growth, the other that we don’t try to position ourselves for some impending doom.

This is also about as far as macroeconomic analysis can take us. In a disaster sure, investment plans are obvious enough, high quality bonds and looking for opportunities to get into blue chips at depressed prices. The absence of a disaster doesn’t quite structure our options for us in the same manner.

We are, sadly, left to investigate specific companies and opportunities for what’s likely to succeed. That the macroeconomy is likely to carry on as it is is that boring which is good. We’re free of a likely disaster that will swamp any microeconomic move, true, but that still leaves us with the more detailed problem of those microeconomic allocations.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.