Shipping market outlook – Container vs Dry bulk : Q2 2022

update

Download the complimentary summary reports

English | Chinese | Japanese | Korean

As of writing (30 May 2022), Capesize rates dropped

significantly and negatively impacted sentiments of smaller

vessels. With an unexpected drop in freight rates, many

long-position players either in FFA or physical have no options but

to cover their position in the FFA market or secure cargo to

near-term position, triggering more downside pressure in the

short-term. However, regardless of the short-term sentiment-FFA

driven rates movement, we believe that the fundamental supply and

demand balance will eventually determine the market.

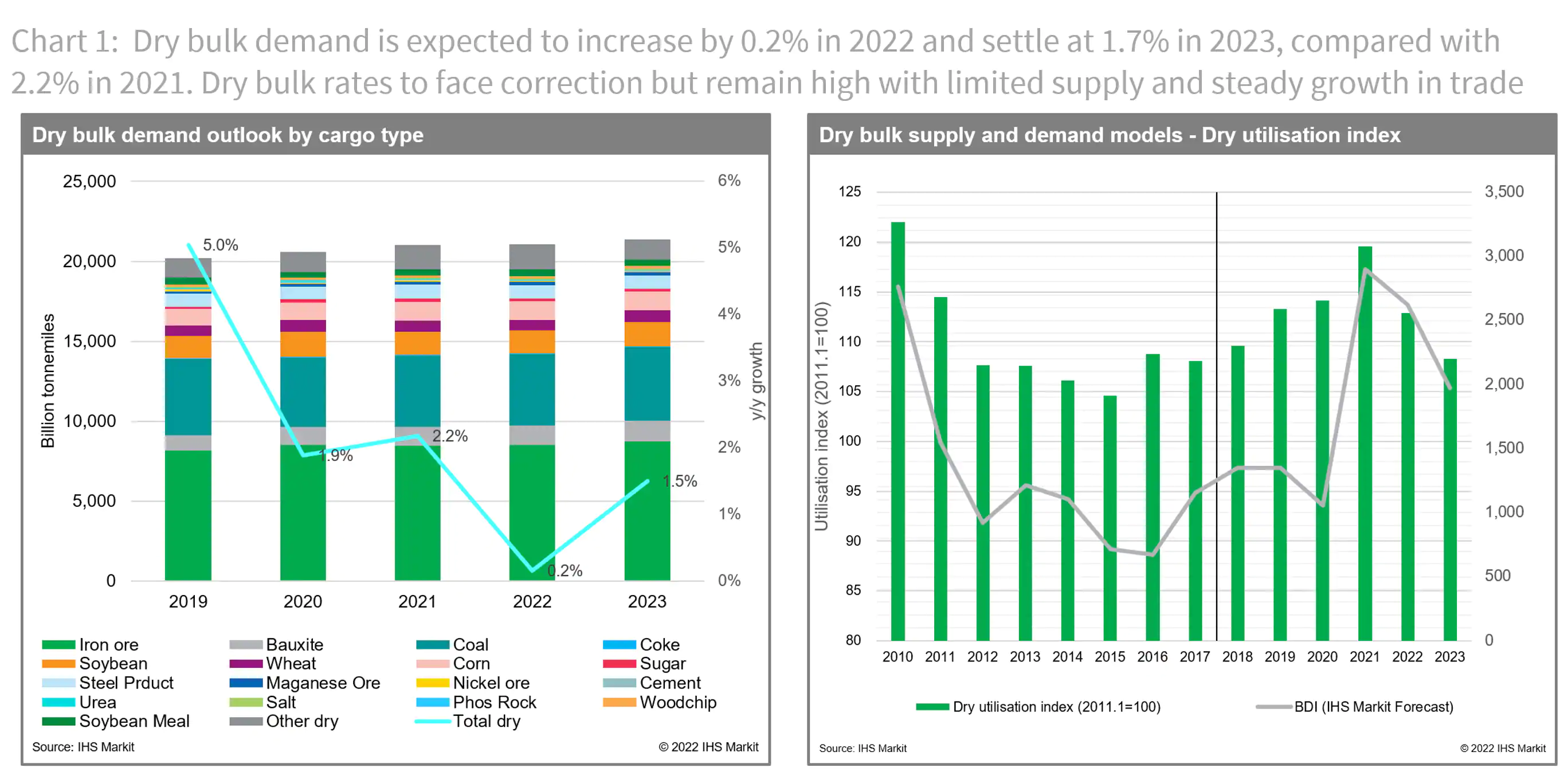

S&P Global Market Intelligence forecasts dry bulk rates to

remain stable in the coming years with limited supply and stable

growth in trade—more bullish in the near-term and bearish for

medium-term. Dry bulk demand growth is expected to decrease to 0.2%

in 2022 and settle at 1.7% in 2023, compared with 2.2% in 2021,

while dry bulk fleet growth will slow to 2.8% in 2022, 2.2% in

2023, and 2.4% in 2024, compared with 3.4% in 2021.

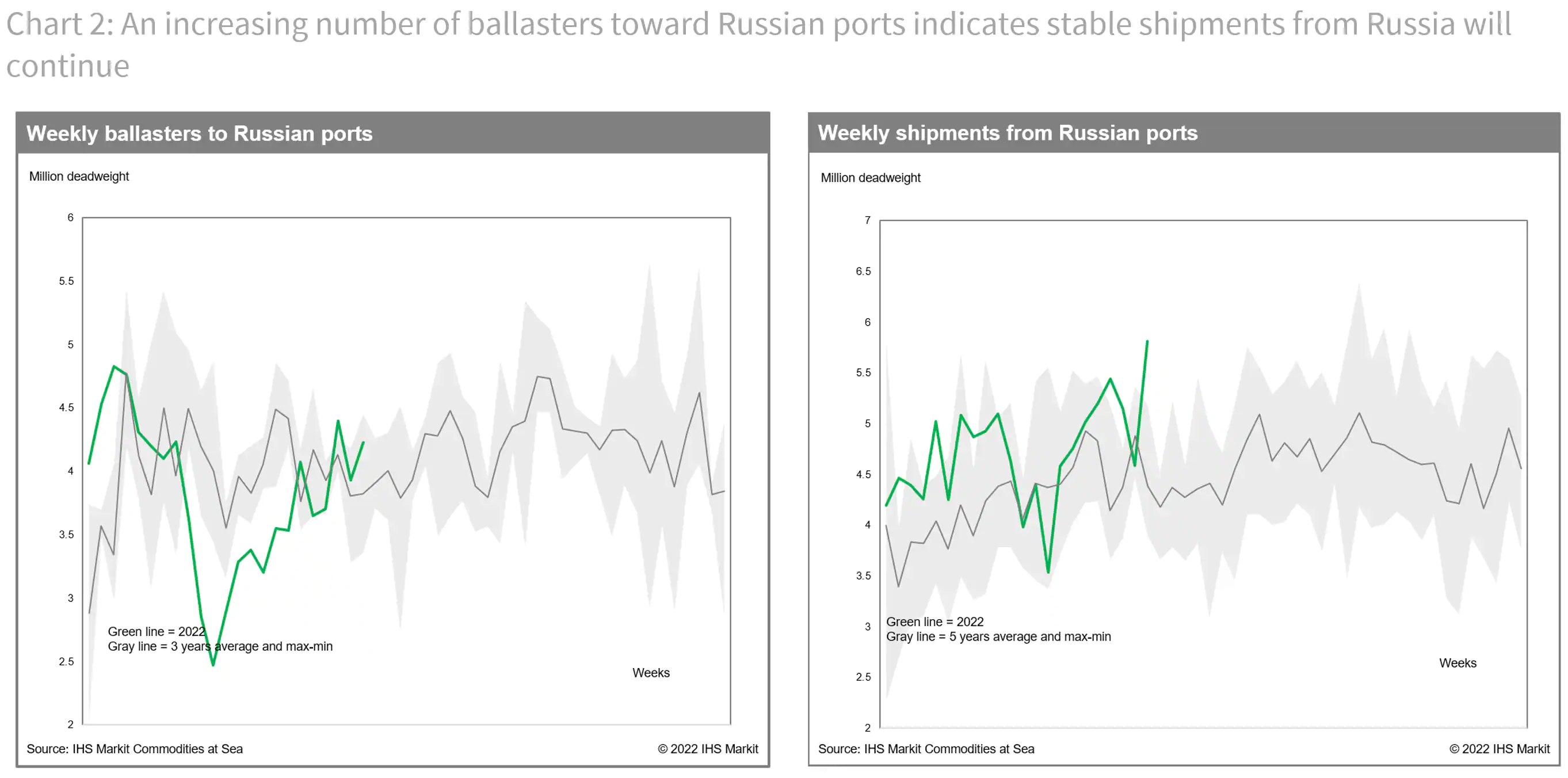

With Commodities at Sea from S&P

Global Market Intelligence, we continue to witness the strength in

Russian cargo shipments; increasing number of ballasters towards

Russian ports indicate the stable shipments out of Russia will

continue before several sanctions, including the European import

ban, which starts in the third quarter. Furthermore, European

demand for Australian coal to prepare for the consequences of

Russian coal import ban, as well as stable minor bulk shipments,

including steel out of the Pacific Basin, is expected to support

backhaul routes in the near-term.

The backhaul remains one of the strongest routes and we expect

it to continue with strength in the container market and

replacement demand for Ukrainian and Russian cargo. We have

consistently argued that as long as container rates remain high

enough to capture part of general bulkers and open hatch cargo

vessels in the container sector commercially, geared bulker rates

are expected to be supported, specifically for backhaul routes.

General cargo (breakbulk) vessels that have shared similar terminal

and cargo with geared bulkers (Supramax and Handysize) have shifted

to the container-linked market because of extremely high freight

rates for container ships this year; container cargo has been

spilling over to general cargo ships (breakbulk/MPV/HL), while

minor bulk cargo usually carried by container or general cargo

vessels have shifted to geared bulkers. Furthermore, with general

cargo ships mostly picking up container-related cargoes, there has

been much less competition from general cargo vessels for

Supramax/Handysize minor bulk routes. These higher demand and

lesser supply balance have boosted geared bulkers’ backhaul rates

even higher.

However, we remain cautious towards the end of the year as we

have observed several downside risks from the later part of the

third quarter of 2022 compared with the same period in 2021.

Specifically, we are tracking the mainland Chinese coal market very

carefully since stronger domestic coal production in mainland China

may eventually limit mainland Chinese coal import demand, which was

one of the main drivers for the strength in the third quarter of

2021. Furthermore, we do not expect extremely high congestion again

in the coming quarters as the result of the easing of COVID-19

restriction. Also, the softening of the container trade growth,

along with high inflation, will be a major risk towards the end of

the year when the third quarter peak season is over.

See the list of risk factors below.

• Softening container market with changing consumer pattern, as

well as weaker purchasing power that will impact smaller segments’

minor bulk demand

• Higher efficiency or productivity of vessels with reduced

congestion and higher speed

• Lower Russian coal demand after the European and Japanese coal

import ban, stronger domestic coal production in mainland

China

• Limited wheat export volume during the Black Sea grain season

DOWNLOAD THE FULL REPORT FOR DEEPER

ANALYSIS COVERING STEEL, IRON ORE, COAL, GRAIN, AND FREIGHT

In this context, S&P Global Market Intelligence Freight Rate Forecast models

predicts Baltic Dry Index (BDI) to increase in the early third

quarter compared with the second quarter with the restocking demand

from Europe before the Russian coal imports ban and seasonal

recovery in shipments as well as continued strength in commodity

prices. However, the dry bulk earning is expected to fall about

20-30% on the year to average about 2,500 – 3,000 points in second

half 2022 with several downside risks, including the major

supply-side impact from the Ukraine-Russia conflict and demand-side

impact from weaker mainland Chinese economy and stronger domestic

coal production and softening container market.

Specifically on the container market impact, we have

consistently argued that as long as container freight rates remain

high enough to capture part of general cargo vessels (multipurpose)

and open hatch cargo vessels share in the container sector

commercially, small geared bulker rates are expected to be

supported, specifically for the backhaul routes. That is why our

major assumption for dry bulk demand and supply has been heavily

linked with the container market outlook.

Currently, we assume container freight rates will also face

correction and decline by 20-30% to average about $6,000-7,000 per

box (FEU) in the second half of 2022 from an average of about

$9,000-10,000 per box (FEU) over the same period last year. The

softening of container trade growth in response to high inflation

rate, endemic consumer pattern, and supply side pressure with heavy

investment in newbuildings, as well as reduced congestion with the

easing of COVID-19 restrictions will be major downside risks in the

second half of the year, specifically after the third-quarter peak

season is over.

Another lockdown in mainland China, slower than expected

economic growth with continued high inflation, and a lack of

stimulus would be a major downside risk, while continued strength

in container freight with high congestion and limited

infrastructure, as well as lower-than-expected domestic coal

production in mainland China and earlier-than-expected reopening of

Ukrainian sea ports would be a major upside risk in our

forecast.

For more insight subscribe to our

complimentary commodity analytics newsletter

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.