Joe Raedle/Getty Images News

This article is contributed by Douglas from our Superstocks Seekers team.

Business Overview

Carvana (NYSE:CVNA), an online used car retailer, has been redefining used car transactions ever since its inception in 2012.

Used car transactions are basically car owners exchanging cars with one another, however due to individuals’ preferences, purchase timings, and also car conditions, direct exchanges can never happen. As a result, several intermediaries were there to facilitate, from dealers buying and holding the used car, financial companies providing loans, to salesmen trying to sell refurbished used cars to potential customers. Each player carries their own risk – inventory risk for dealers & credit risk for financial companies – thus requiring certain markups to ensure profitability. All these trickle down to the end consumer ultimately paying a higher price and usually getting upsold by the salesmen after spending hours at the dealership.

What Carvana is trying to achieve is to improve the whole customer experience by vertically integrating the relevant functions, and making the purchase journey an easy and enjoyable one. And of course, the cheaper option too.

Following In The Footsteps Of An Online Giant

Every decision Carvana chooses to take is based on improving customer experience. From the start, choosing the e-commerce model for car sales was not easy since test drives are key to car buying. They overcame this by offering an unprecedented 7-day free return policy. It not only allows customers to test drive cars on their own time with no pressure from salesmen, but they can also even choose to return the cars if they don’t like it.

This policy is reminiscent of that of Zappos, the online shoe and apparel retailer that prides itself on its customer service. They are known for delivering multiple shoes to customers for them to try, and then taking back the unwanted ones, at no additional costs. Their success in customer focus was what led to them being acquired by Amazon (AMZN) – the epitome of customer obsession.

The logistics networks that Carvana is building up over the whole USA, its own transportation fleets, Vending Machines (“VM”) and Inspection & Reconditioning Centers (“IRC”), are aimed at offering faster deliveries to customers. It’s similar to that of Amazon, by laying out the fixed costs so that variable costs will be low at scale, which in turn lead to even lower prices for customers. Also, by controlling every aspect of operations, Carvana can better control the service quality, ensuring that the overall customer experience is not being brought down by any external parties. A chain is only as strong as the weakest link, as long as there’s a weak point (e.g. 3rd party delivery driver being rude), the customer will view it as a bad experience.

Carvana’s founder/CEO Ernie Garcia III has the same mental model as Amazon’s founder/former CEO Jeff Bezos. Instead of predicting what customers might want in the future, why not just focus on what customers are always looking for – Lower prices, faster delivery, and a fun & easy experience. That’s what spawned the idea of the VM, which enables customers to pick up their car in a novel way while lowering the overall last-mile delivery costs. The bright lights of the infrastructure, coupled with its branded transportation fleet, also help with establishing a strong brand presence.

Source: Bay Area’s New Vending Machine

Improving Results at ever rising costs?

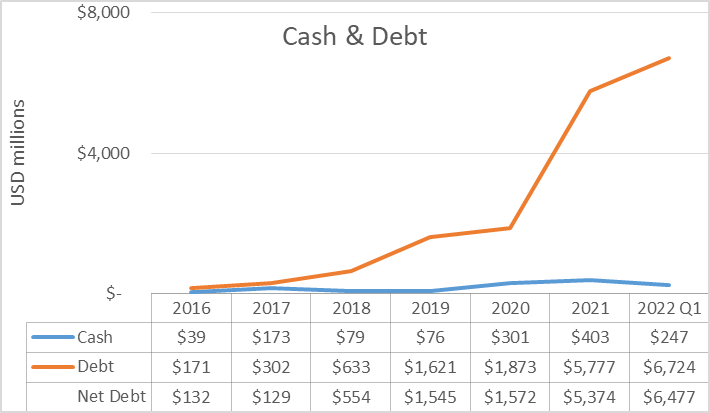

Though this helps Carvana to differentiate itself, all these investments in assets are putting a toll on Carvana’s balance sheet. Its capital intensive business requires a non-stop infusion of cash, and Carvana simply doesn’t have sufficient cash-generating ability from its operations yet.

Source: Own chart using data from SEC Filings

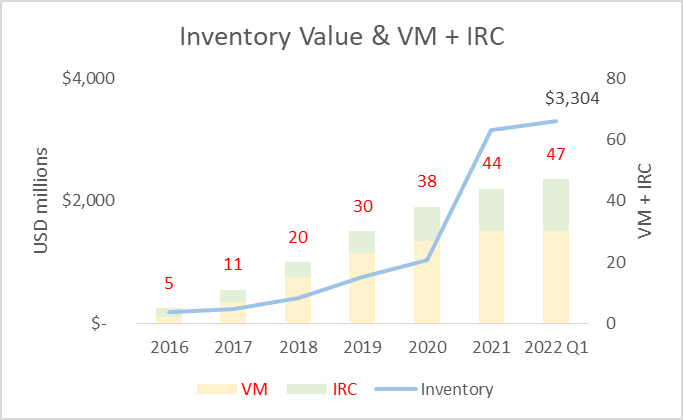

Source: Own chart using data from SEC Filings

As illustrated from the above charts, capital raised from debt has been channeled into building up its inventory and logistics network. In order to be a successful nationwide e-commerce platform, Carvana has to have ample inventory spread out across its various IRCs. Otherwise, customers will not find what they want or they will be unsatisfied with the long delivery times, both not adding value to the customer experience. Even with a vertically integrated model, inventory costs are still going to increase with scale, which readers have to take note of. In addition, used car prices have been increasing and Carvana is purchasing them at higher prices. Even though they are still cheaper than those sourced from auctions, inventory risk will only get larger if recession hits and sales slow down, which will result in increased credit exposures. Being vertically integrated might be more cost-efficient, but it also means that the company is exposed to all the risks that different stakeholders would have faced in other companies.

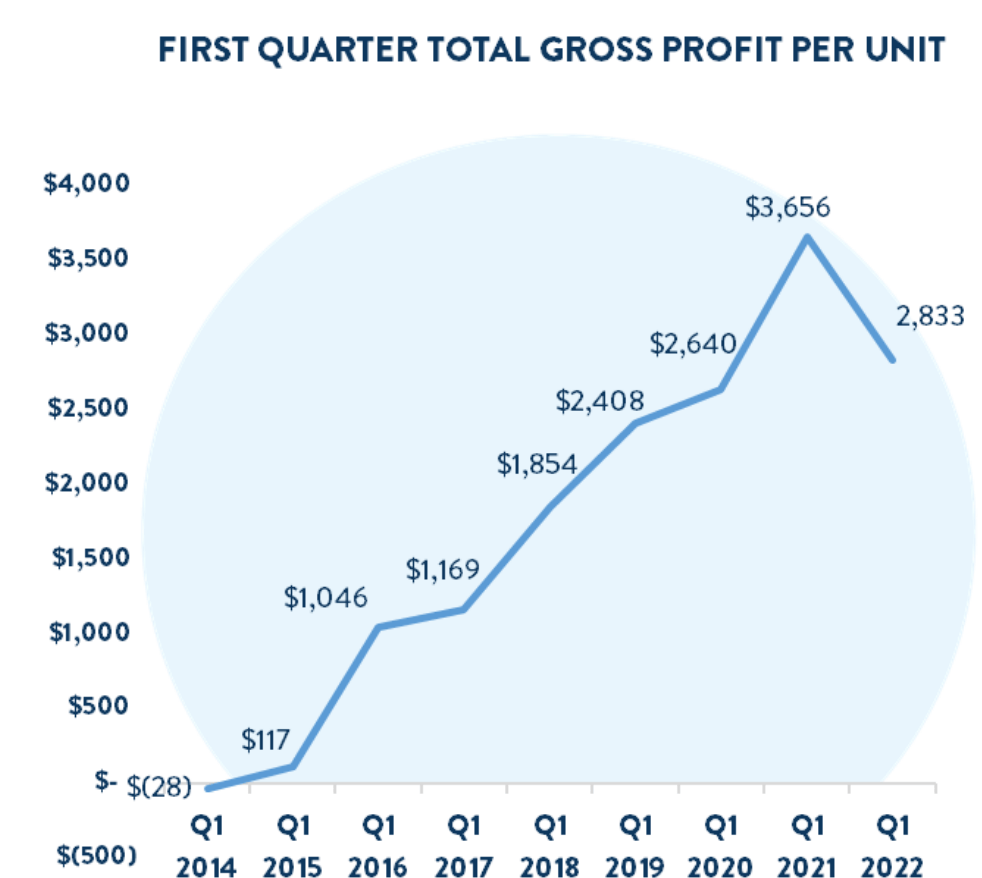

However, all’s not doom and gloom yet. Total Gross profit per Unit (“GPU”) has been improving every year, despite the dip in the recent quarter. CEO Garcia mentioned that Q1’22 was a challenging quarter for them as sales came in lower than forecast, coupled with an increased purchase price, leading to increased costs per retail unit sold. The unit expenses can be further optimized now with the ADESA acquisition which can help lower transportation costs, which might help in improving profitability.

Source: Q1’22 Shareholder Letter

ADESA Acquisition

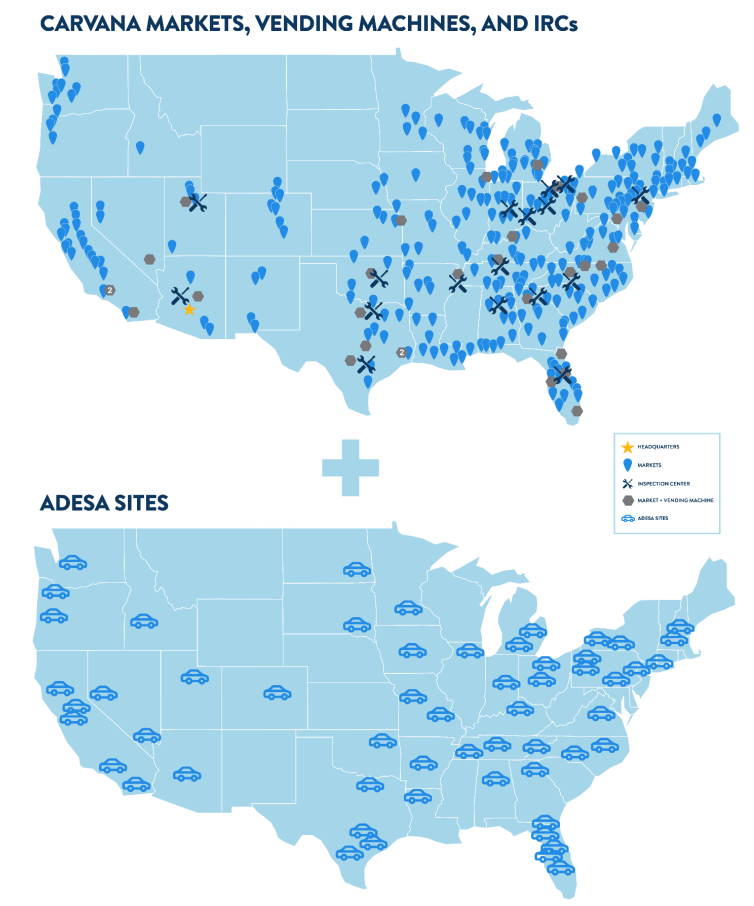

The ADESA acquisition announced in Feb’22 was priced at USD 2.2 billion in cash. This also led to further capital raising, with the company raising $4.5billion from debt and equity. This signaled a “Go big or go home” intent from the company. The below picture illustrates the rationale behind the acquisition.

Source: Q1’22 Shareholder Letter

ADESA auction sites can serve as a basic repair center for now, and a full-scale IRC in the future when they are developed according to Carvana’s standards. More importantly, it expanded Carvana’s network coverage, allowing them to be closer to end consumers and thus lowering transport costs. This clearly accelerated the company’s growth trajectory, as compared to them going through the cycle of sourcing & securing individual sites and building IRCs up from scratch site-by-site. Furthermore, wholesale vehicles can now be transported straight to auction sites, instead of going from source to IRC to auction sites.

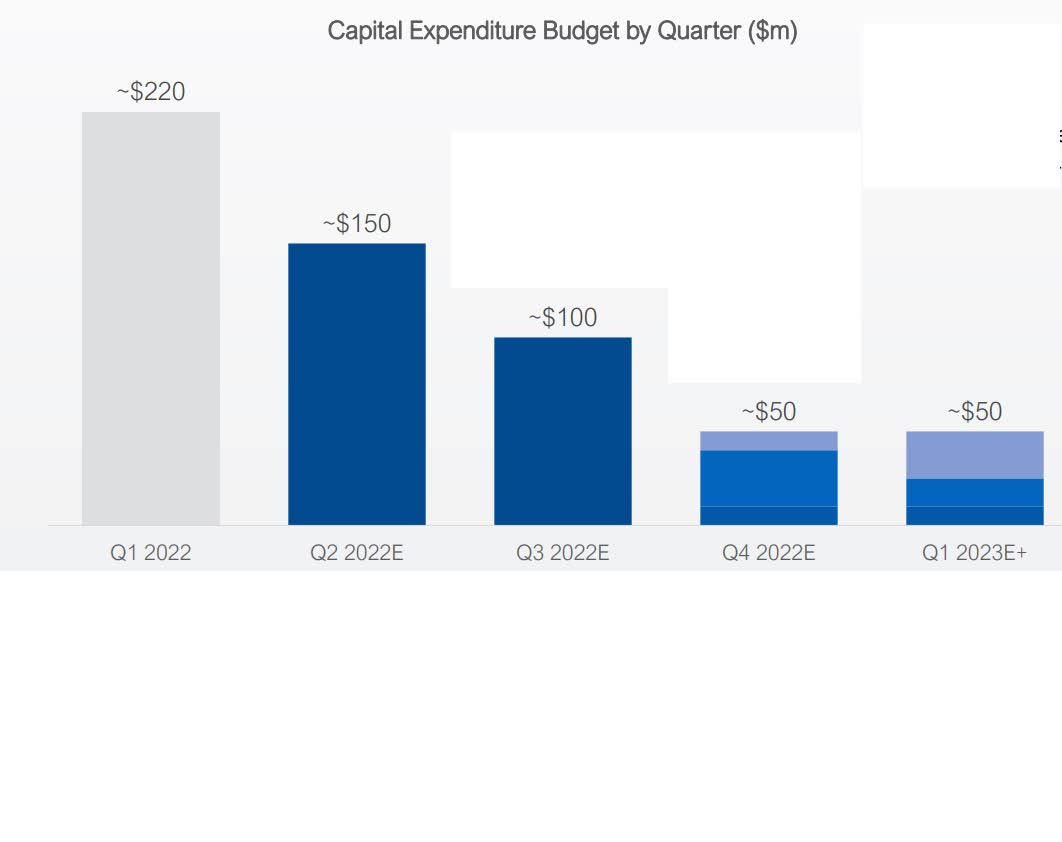

Source: May’22 Operating Plan Updates

With the company forecasting a huge CAPEX reduction over the upcoming year, it’s signaling a halt to develop new IRC sites. From here on with economies of scale, more profits will flow to the bottom line, with promising signs of free cash flow (“FCF”) potential. The last time they had a less than $50m CAPEX quarter was in Q2’19, when they had only 7 IRCs.

Snippets from the CEO

In one of his YouTube interviews, CEO Garcia stated that he only owns a Volvo. To me, it speaks volumes when the owner of a car dealership doesn’t own multiple cars when they are so readily available to him. With such a down-to-earth man at the helm, Carvana just doesn’t smell like a fraudulent company. He mentioned in the same interview that if it’s all about making a lot of money, he would have started a marketplace business instead of a vertically integrated one.

In addition, during the Wells Fargo Summit in Dec’21, when asked to choose between a higher unit sales or a higher margin in the upcoming year, he chose to have a higher unit sales even if margins don’t show up yet. It matches closely with his ultimate goal of being the top used car dealer in the uber fragmented industry, and showing great margins at the current phase is not going to be helpful in the long run. The CEO seems to be very clear on the growth trajectory despite taking on increasing amounts of debt, displaying huge confidence in the business.

Valuation

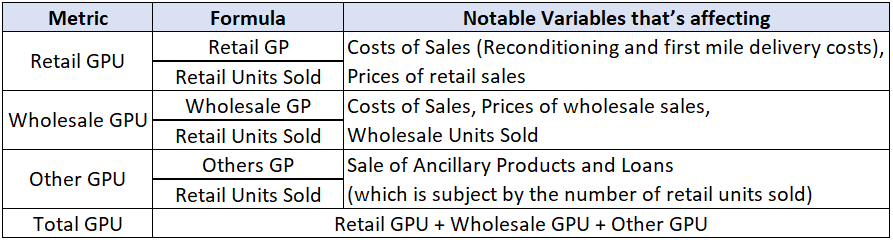

For valuation purposes, I will be using CarMax’s (KMX) financials as a reference since they are the top used car dealer in the country. As per the recent financial year, CarMax has a Retail GPU of $2.2k & Total GPU of $3.6k, as compared to $1.6k & $4.5k for Carvana. (Refer to the below table for a brief overview of the metrics.)

Source: Author’s table

This shows that Carvana still has room to grow in optimizing its cost of sales. Also, Carvana has a more profitable finance business from its loan securitisation. With more efficient use of assets & increasing its wholesale sales, I believe that Carvana will be able to sustain a $4.5k total GPU over the long-term while still keeping prices lower than competitors, even if loan performances falter.

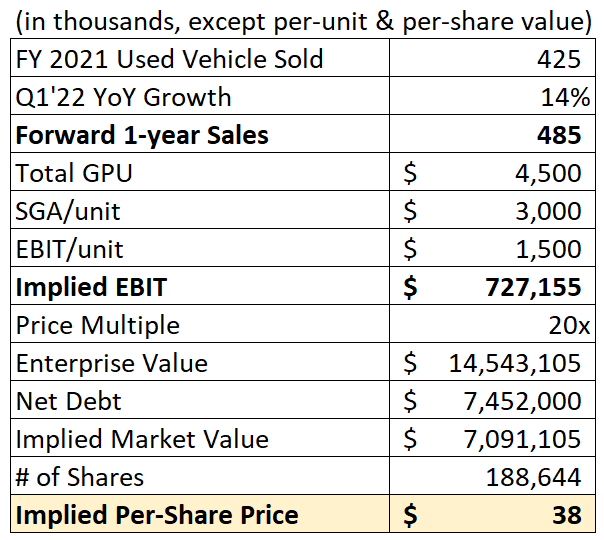

Secondly, the management has set a mid-term goal of $3k for SG&A expenses/unit. Thus, I am using that as a guide since the company is not operationally profitable yet.

For the price multiple, CarMax has been trading at 20-25x of Earnings before interest and tax (“EBIT”) for the past 5 years. A 20x multiple is used for the below valuation as Carvana is still in the midst of scaling.

Source: Author’s estimates

After taking into consideration the capital raises and share offering, I derived an intrinsic value of $38/share. This is portraying a bull-case scenario where Carvana is operationally profitable. There is certainly an upside from here if the company manages to achieve these economics in the near future while growing at a higher rate.

Risks

The most apparent risk will be the company’s balance sheet. Continuous capital raising is both putting the company at risk in bad times and dilutive to shareholders. Especially in current times when interest rates are projected to increase in the near future, management has to tread this line very carefully.

Secondly, inventory risk. The rapid depreciative nature of cars’ value makes holding on to inventory for prolonged periods more dangerous for the company. Even more so now when cars are being purchased at higher prices, Carvana has to cherry-pick the correct models to acquire. This links back to the rationale behind the acquisition. With more sites around the country, the turnaround time from acquisition to inspection & repair works to being made available for sales can be shortened.

FBC (Fulfillment by Carvana)?

By looking at what Amazon is doing, there seem to be so many optionalities for the company in the future. With all these infrastructure and logistics networks in place, Carvana can easily become a 3rd-party service provider for other car dealers, or even partner with automakers. Its e-commerce platform can also serve as a marketplace for dealers without an online presence. This is already being explored by the company through the partnership with Hertz.

Closing

Carvana has the right business model to succeed. Being in a fragmented industry will definitely help capture market share rapidly once its nationwide hub-and-spoke model is up to scale. It’s now up to the management to step on the gas pedal to show that a pure e-commerce model can work for vehicle sales too. Buying at current prices is equivalent to putting full faith in the management, that they know their economics and not just playing with fire by growing at all costs.