If you want to know who really controls Creative Peripherals and Distribution Limited (NSE:CREATIVE), then you’ll have to look at the makeup of its share registry. Large companies usually have institutions as shareholders, and we usually see insiders owning shares in smaller companies. I quite like to see at least a little bit of insider ownership. As Charlie Munger said ‘Show me the incentive and I will show you the outcome.

With a market capitalization of ₹1.2b, Creative Peripherals and Distribution is a small cap stock, so it might not be well known by many institutional investors. In the chart below, we can see that institutions don’t own shares in the company. We can zoom in on the different ownership groups, to learn more about Creative Peripherals and Distribution.

See our latest analysis for Creative Peripherals and Distribution

What Does The Lack Of Institutional Ownership Tell Us About Creative Peripherals and Distribution?

Institutional investors often avoid companies that are too small, too illiquid or too risky for their tastes. But it’s unusual to see larger companies without any institutional investors.

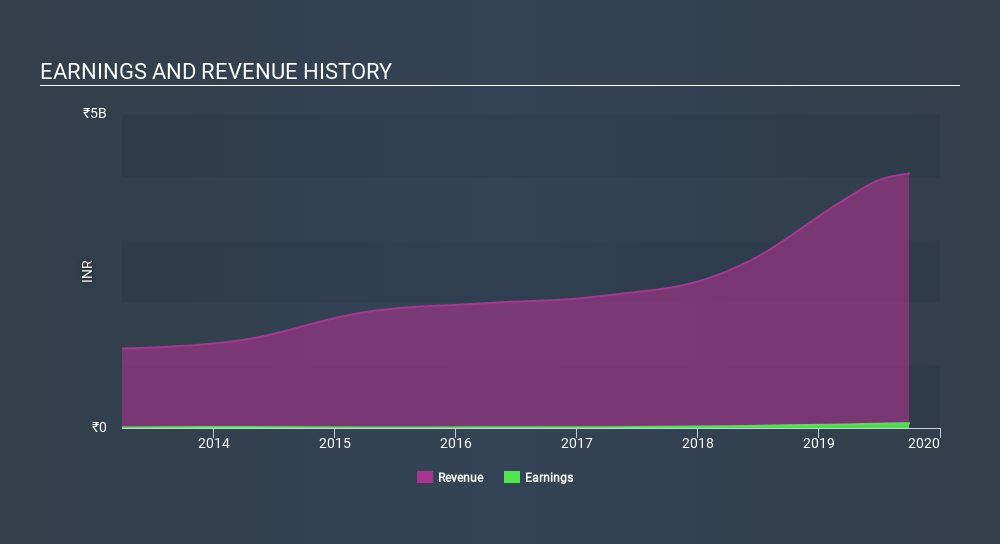

There are multiple explanations for why institutions don’t own a stock. The most common is that the company is too small relative to fund under management, so the institition does not bother to look closely at the company. Alternatively, there might be something about the company that has kept institutional investors away. Institutional investors may not find the historic growth of the business impressive, or there might be other factors at play. You can see the past revenue performance of Creative Peripherals and Distribution, for yourself, below.

Creative Peripherals and Distribution is not owned by hedge funds. The company’s CEO Ketan Patel is the largest shareholder with 68% of shares outstanding. This implies that they possess majority interests and have significant control over the company. Investors usually consider it a good sign when the company leadership has such a significant stake, as this is widely perceived to increase the chance that the management will act in the best interests of the company. The second and third largest shareholders are Jayantilal Lodha and Vikram Lodha, holding 2.6% and 2.2%, respectively.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock’s expected performance. As far I can tell there isn’t analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of Creative Peripherals and Distribution

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

Insider ownership is positive when it signals leadership are thinking like the true owners of the company. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances.

Our information suggests that insiders own more than half of Creative Peripherals and Distribution Limited. This gives them effective control of the company. So they have a ₹960m stake in this ₹1.2b business. When analysing a company, looking at ownership may seem a logical place to start. But ultimately, many risks exist within the business itself, rather than its shareholders. For example, we’ve discovered 4 warning signs for Creative Peripherals and Distribution (of which 1 is major) which any shareholder or potential investor should be aware of.

General Public Ownership

With a 20% ownership, the general public have some degree of sway over CREATIVE. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Next Steps:

I find it very interesting to look at who exactly owns a company. But to truly gain insight, we need to consider other information, too.

I like to dive deeper into how a company has performed in the past. You can find historic revenue and earnings in this detailed graph.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

If you spot an error that warrants correction, please contact the editor at [email protected]. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

These great dividend stocks are beating your savings account

Not only have these stocks been reliable dividend payers for the last 10 years but with the yield over 3% they are also easily beating your savings account (let alone the possible capital gains). Click here to see them for FREE on Simply Wall St.