blackdovfx/E+ via Getty Images

RLI Corp (NYSE:RLI) is a company that we’ve been following for a while now. It was brought to our attention due to the excellent track record and more marginal markets of niche coverage and personal umbrella insurance. The less covered markets, we thought, offered it pricing power ahead of other insurers, where insurers already have a decent amount of pricing power, making them attractive in an inflationary environment. RLI continues its tradition of profitability with topline growth very likely to be sustained thanks to a recovery in public transportation, but also with inflation and supply chain complexity driving demand in excess liability insurance in construction and specialty auto. With a reversion to the mean in P&C losses coming relative to tough hurricane and storm years just recently, the profits look promising, but the multiple is already quite fair, although more compelling than before.

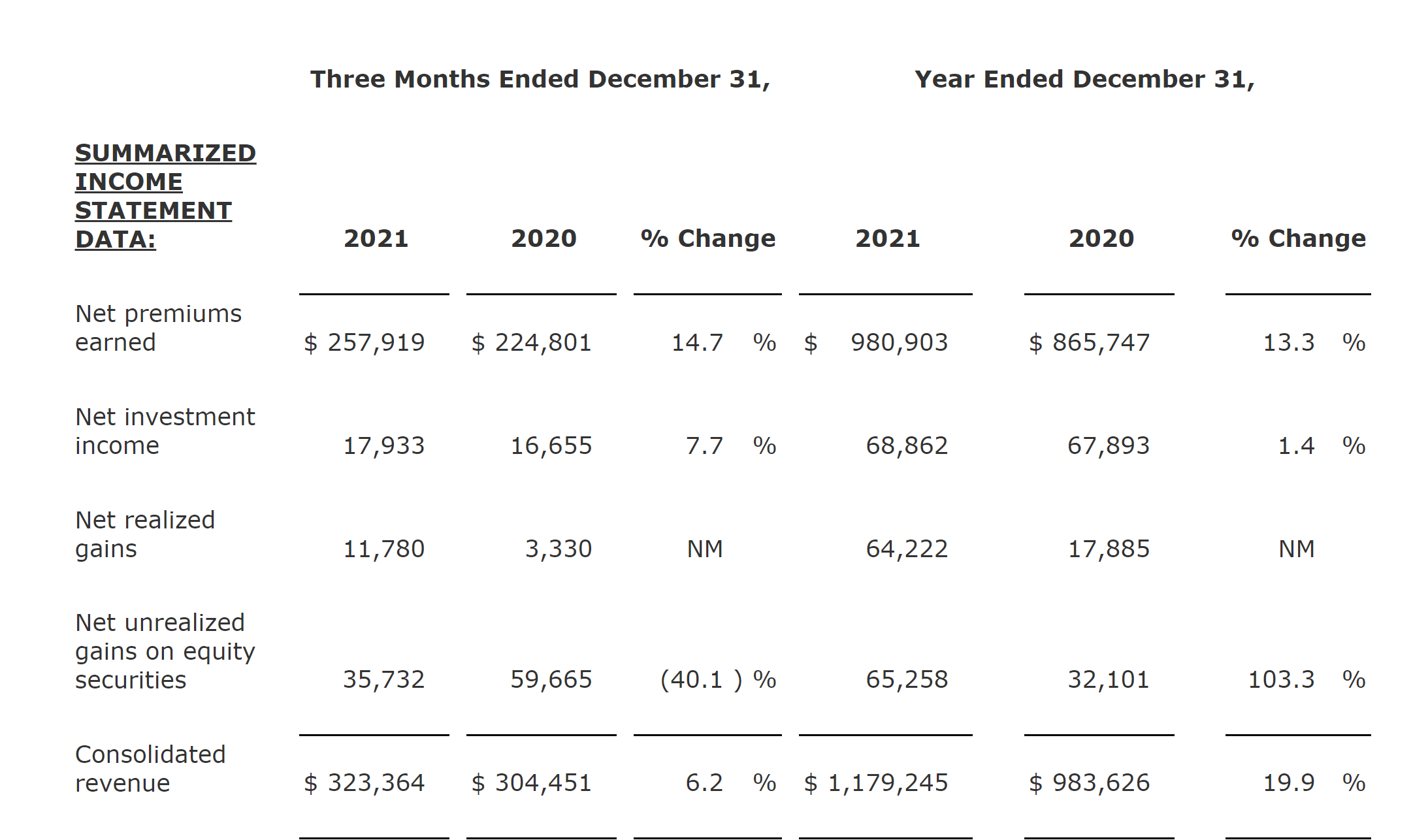

A Look At Q4

Q4 was characterised by decent topline growth. This is mainly coming from the recovery in public transportation, which RLI provides specialty insurance for. Moreover, tougher weather conditions and the substantial damage that came in the last couple of years has been a reason for people to buy RLI’s specialty insurance plans and personal umbrella insurance to cover those quite costly risks. Supply chain and logistics concerns has also supported demand for excess liability insurance in the construction industry. So overall, topline growth has been strong in the wake of damages from prior years.

RLI Earnings FY 2021 (RLI Q4 2021 Pres)

Moreover, the lack of damages this year has meant improved profitability too, with combined ratios falling meaningfully and profits continuing their rise.

Note on Inflation

However, we are seeing inflation, and the environment could mean greater negative outcomes might materialise for RLI. While pricing power affords RLI the opportunity to stay ahead of inflation by raising premiums, inflation is also affecting the premiums for reinsurance that RLI takes on. Moreover, inflation in building materials and housing prices, combined with the strained supply chain environment, means the plans are larger in the construction business than before, which is positive, but so are the potential claims in terms of size and probability. With RLI covering excess liability on construction, supply chain risk is exactly the risk they are taking on in those businesses. Moreover, with specialty auto insurance for rental car companies and such, there is the issue that auto repairs take longer than expected because of the strained environment, which again incurs claims on RLI.

Conclusion and Valuation

While the performance was good last quarter, and we’ve seen earnings growth, it is somewhat due to a suspension of effects that might be coming in from inflation. However, there is no question that there is topline growth, and inflation has to do with that both directly and indirectly through RLI’s ability to increase premiums in niche markets to stay ahead inflation. The fundamentals remain good, and the special dividend of $2 per share, getting this year’s annualised yield up to 3%, is a reflection of that. At the 16.5x P/E multiple, while not remotely excessive, reflects the situation of RLI fairly well. For us, not compelling enough, but for investors looking for Buffett-style quality, with an amazing track record of profits and earnings growth, the price is indeed fair and RLI could be attractive. Still, we rate it neutral.

If you thought our angle on this company was interesting, you may want to check out our service, The Value Lab. We focus on long-only value strategies, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our group of buy-side and sell-side experienced analysts will have lots to talk about. Give our no-strings-attached free trial a try to see if it’s for you.