Kimberly White/Getty Images News

My advice for a down market: pick some “forever stocks” that are currently trading down versus their peaks, scoop them up at a discount, and hold your nose for the eventual rebound. Over the past month, it has felt like the sky is falling for the tech sector with many high-flying names losing 40-50% of their value. Now is not the right time to reduce your portfolio allocation to tech, however. Instead, focus on shifting more allocation to the value-oriented names within the tech sector.

Oracle (ORCL) is a shining example of a prudent investment during these choppy times. The database giant, long one of the tech stalwarts of Silicon Valley, continues to impress through its combination of both cloud growth and sustained earnings power.

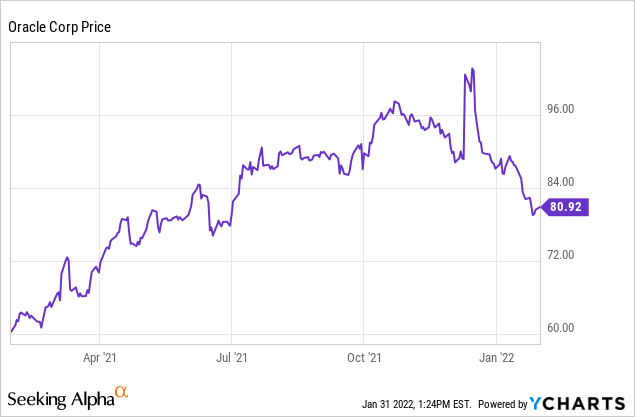

It’s down a lot less (20%) from peaks than some of its flashier tech peers. Oracle stock is down largely for two reasons: one, the general sentiment building against tech stocks, and two, the recent announcement of Oracle’s plan to acquire Cerner for $28.3 billion.

While the largesse of the deal certainly produced some sticker shock as one of the most expensive acquisitions in the software sector (though Microsoft (MSFT) came out in January with its proposed $68.7 billion all-cash bid for Activision Blizzard (ATVI), which has been in the spotlight for workplace culture issues – certainly this has removed some of the shock value of the Oracle Cerner deal), I lean toward a favorable attitude on the Cerner deal.

For one – Cerner is already an established leader. Its technology and devices are used across the globe, and because it’s profitable, it will immediately be accretive to Oracle’s bottom line. Second, as Oracle CEO Safra Catz describes it, healthcare is the most important vertical in the world – and it is rarely disputed that it’s the industry that is most ripe for disruption by technology. With this massive foothold on the healthcare industry now, Oracle has a solid shot to chase its next leg of growth through innovation in healthcare.

Overall, I remain bullish on Oracle, especially with the dip from peaks that we’ve seen since the Cerner deal was announced. In my view, the bullish thesis for Oracle still remains well intact:

- Oracle’s portfolio is broad and covers every spectrum of enterprise technology. Oracle now has a full suite of front-end applications covering functions such as supply chain, finance, HR, sales – everything under the sun. The company has also retained its traditional strength in backend infrastructure, with products like the Oracle Autonomous Database. Not all of Oracle’s products have to be winners: at the moment, cloud apps continue to see 20-30% growth, offsetting declines in legacy segments.

- Sales machine. Oracle essentially invented the sales playbook in Silicon Valley. Its late co-CEO, Mark Hurd, is often credited with institutionalizing the position of a “business development representative”, the cold-calling army that now represents among the most common entry-level positions in the industry. Oracle has among the best-oiled sales processes in enterprise technology, and continues to leverage that playbook to grow its business.

- Profitability has long been core to Oracle’s DNA. Oracle has retained enormous profitability, even with its shift to cloud and away from lucrative license/maintenance contracts. Its mid-40s pro forma operating margins are among the highest in the software industry.

- Recent personnel decisions could boost profitability. More to that point, Oracle’s decision to move its headquarters from Redwood Shores (a small town in the San Francisco Bay Area that is almost exclusively dedicated to Oracle’s headquarters) to Texas could help lower Oracle’s overall personnel costs. It has also announced a flexible remote work policy that is also slated to reduce overhead (Larry Ellison himself has committed to working out of Hawaii for the time being).

- Big buybacks. Oracle has been a big proponent of utilizing its considerable balance sheet to return capital to shareholders. Over the last ten years, Oracle has managed to bring down its shares outstanding by a considerable 46% (compare that to many newer software startups, which issue new stock like candy and continue to grow at all costs by raising secondaries and using stock to buy out competitors).

Oracle’s valuation is also looking quite modest as well. For FY23, which for Oracle represents the fiscal year ending in July 2023, Wall Street analysts are expecting the company to generate $5.26 in pro forma EPS, representing 9% growth over consensus FY22 EPS of $4.82. Against this earnings outlook, and at current share prices near $81 at the time of writing, Oracle trades at a modest ~15.4x FY23 P/E ratio, a discount to the broader market.

In short, I continue to view Oracle as an enterprise software titan that continues to hold a massive recurring revenue base and constantly re-invents itself, both through organic growth and transformative acquisitions like Cerner. Its valuation is well supported by its earnings, and as such I think a near-term rebound and outperformance versus the broader market is very likely.

Q2 download

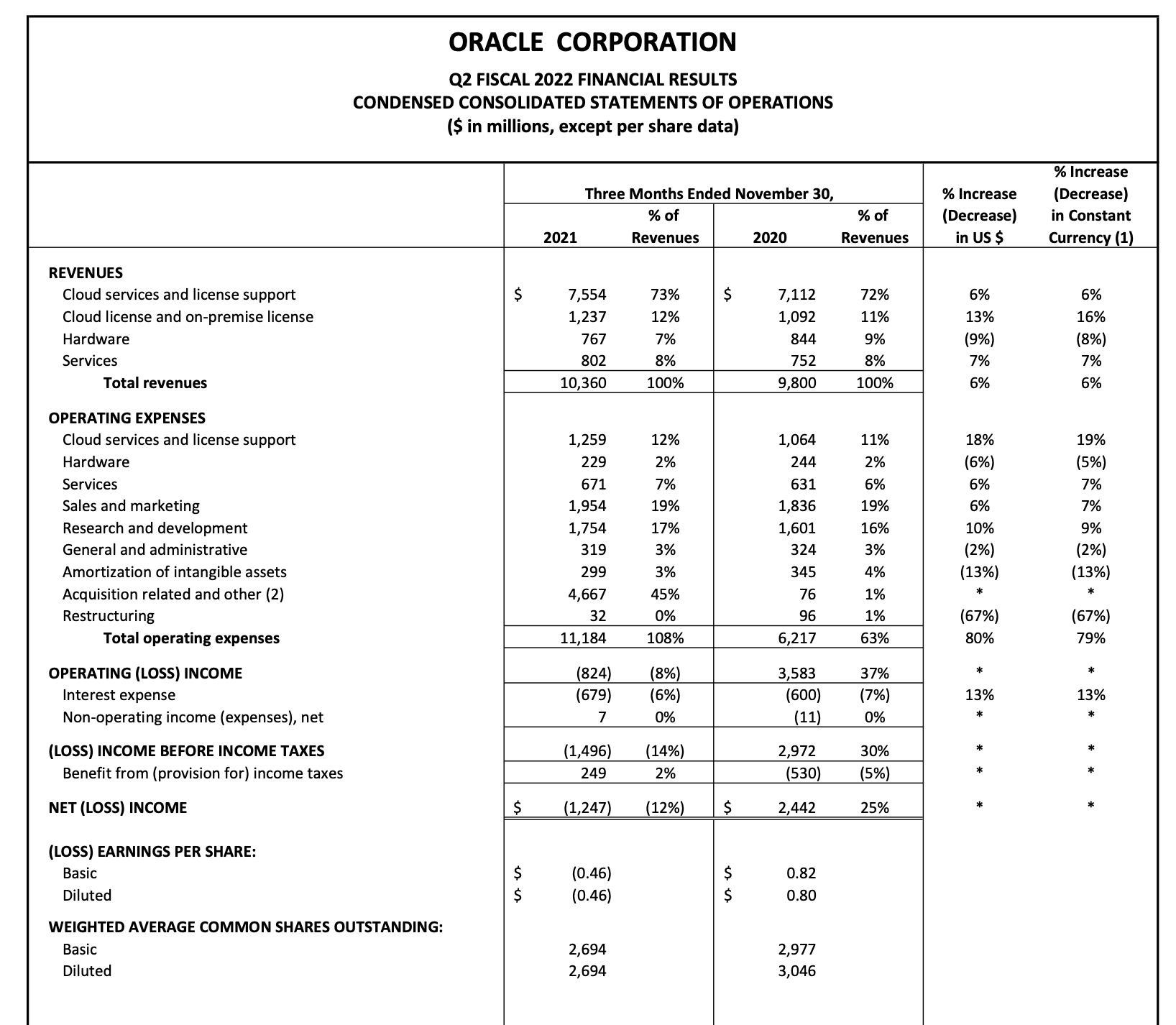

Let’s now go through Oracle’s latest fiscal Q2 results (covering the quarter for Oracle through November), released in early December, in greater detail. The Q2 earnings summary is shown below:

Oracle Q2 results (Oracle Q2 earnings release)

Oracle’s revenue in Q2 grew at a 6% y/y pace to $10.36 billion, beating Wall Street’s expectations of $10.21 billion (+4% y/y) by a two-point margin. It’s also worthwhile to call out that the company’s revenue accelerated two points versus 4% y/y growth in Q1.

Looking ahead, Oracle expects to continue plugging away at full steam. The company is expecting now to end the full fiscal year at a “high mid single digit” total revenue growth rate, with cloud revenue growth (which it no longer routinely breaks out separately from on-prem licenses) exiting the year at a >20% y/y growth pace. For Q3 specifically, revenue is expected to grow at a 6-8% y/y total pace, with the midpoint of that range suggesting further acceleration.

Here’s some helpful anecdotal commentary from Oracle CEO Safra Catz on the drivers behind that acceleration:

Before I go through the numbers, though, I wanted to comment on what we are seeing in the market that is driving our accelerating revenue growth. As I’ve mentioned on previous calls, we have a highly differentiated strategy from our competitors where we are the only company able to offer the combination of applications and infrastructure in the cloud.

We have best-of-breed capabilities in both infrastructure and apps like HR and ERP, but also a highly differentiated set of industry-specific cloud SaaS applications and of course, our second-generation cloud with Autonomous Database are unique in their performance, security and dependability. And because we have decades of experience in mission-critical systems, our customers can depend on us being up and available when they need us.

Our unique capabilities are attracting customers, especially as they consider how to conduct their own digital transformation in the complex industries in which they compete. They want us to know as much about their business as they do, whether it’s telco, financial services, utilities, retail and many others and to partner with them to modernize.”

The company’s core cloud apps all continued to see strong growth as well. The Fusion lineup of enterprise software cloud tools is up 30% y/y in the second quarter, with ERP up 35% y/y and HCM up 25% y/y. Both of these categories are the stronghold of Workday (WDAY), which many investors don’t realize was founded by an ex-Oracle staffer. Workday’s revenue, meanwhile, has flattened out to a 20% y/y growth pace – suggesting that after years of lagging, Oracle’s Fusion products are finally gaining market share over its decades-long rival. Additionally, NetSuite, Oracle’s ERP system for mid-market clients that it acquired in 2016, saw strong 28% y/y revenue growth.

Oracle’s pro forma operating income, adjusting for acquisition-timing related expenses, also grew 7% y/y to $4.86 billion, representing a very rich 47% pro forma operating margin. Oracle continues to expect improved leverage in its cloud business, with growth in gross profit dollars accruing from cloud expected to be better than in FY21.

The company’s pro forma EPS, meanwhile, grew 14% y/y to $1.21, which came in ahead of Wall Street’s expectations of $1.11, which matched the company’s internal guidance last quarter. Oracle’s board also approved an additional $10 billion adder to its buyback authorization, which at Oracle’s current market cap of ~$220 billion covers just shy of 5% of the company’s outstanding market cap. It’s a prudent time, in my view, for Oracle to be buying back shares when its stock is trading at only ~15x 2023 earnings.

Key takeaways

Oracle remains a highly diversified multi-product software vendor whose opportunity landscape has expanded dramatically with the addition of Cerner sometime in 2022. Trading at a very modest multiple of forward earnings, Oracle offers a great chance to remain invested in cloud/technology while avoiding paying steep valuation multiples. Stay long here.