Editor’s note: Earlier this year the Special Projects team at AspenCore Media began compiling articles for a comprehensive report on the electronics supply chain. Although that project was delayed — this is the supply chain, after all — the content provides an in-depth snapshot of the year that was. This is part of our Special Report.

Editor’s note: Earlier this year the Special Projects team at AspenCore Media began compiling articles for a comprehensive report on the electronics supply chain. Although that project was delayed — this is the supply chain, after all — the content provides an in-depth snapshot of the year that was. This is part of our Special Report.

It’s fair to say that the supply chain in 2021 didn’t evolve as expected. A chip shortage at the beginning of the year has only gotten worse; global logistics are hopelessly backlogged; prices are on the rise and a new variant of Covid-19 is emerging. Despite this, the U.S. manufacturing sector has expanded for 18 months and demand remains high.

Foreign markets are also rebounding after a sluggish start. According to the IPC, China’s recovery began in mid-2020 and posted a positive growth rate of 2.3 percent for the year, the only major economy to achieve positive GDP growth. Forecasts for China’s growth rate for 2021 ranged between mid-7 percent and mid-8 percent.

IHS Markit forecast a robust 5.6 percent GDP growth for the U.S. economy in 2021, thanks in large part to the $1.9 trillion American Rescue Plan Act. Europe has lagged both China and the U.S. in GDP growth. It experienced a much slower pace of economic recovery due to lingering Covid-19 fallout in early 2021 and smaller stimulus packages than the U.S.

Businesses have been planning for a “new normal” following the pandemic but the chip shortage has derailed any sense of normality. Moreover, there’s a sense that there has been a fundamental shift in the way companies view the interconnected global economy.

Covid-19 has been the catalyst for many companies to re-examine the structure and performance of their global supply networks. Supply chain resilience has become a hot topic in boardrooms as companies question whether the focus on efficiency and the just-in-time philosophy of production, which has been gospel since the 1980s, is really the best way forward.

The semiconductor shortage is an excellent example of why these discussions are taking place. A slowdown in 2020 led to cancelations of component orders that rippled through the electronics component supply chain. When production picked up, the inventory on hand of the much-needed semiconductors was lagging demand. Lead times stretched out and prices skyrocketed. In the U.S., GM, Ford and other automakers made headlines as they shut down production because of chip shortages.

Covid-19 may have been the catalyst for the semiconductor shortage. But the fix is more complicated than a vaccination. It will take more than a few months or a few years to establish a stable and sustainable new normal for global supply chains.

What’s shaping the new normal?

Three factors will have an outsized influence on the performance of global supply chains in the coming years: Geopolitics, climate change, and cybersecurity.

- Geopolitics

Consider the U.S.-China trade war initiated by the Trump Administration, which entered its third year as the Covid-19 pandemic hit. The tariffs were intended to cow China into submission but instead drove up the cost of imports, including electronic components and products. The Biden Administration has kept the tariffs in place.

China’s failure to acquiesce to U.S. pressure was a stark reminder of how far the relationship between the two countries has come since China was admitted into the WTO in 2001. China is a world power in terms of economic and military strength. A recent projection by Nomura suggested that China’s GDP would overtake the US in 2028. China has taken control of Hong Kong

In March, former Google CEO Eric Schmidt, speaking at a National Security Artificial Intelligence Conference, said the U.S. government and the technology industry need a new approach for artificial intelligence (AI), microelectronics and other critical military innovations to maintain technology advantage over China. Keeping things as they are “is not going to work,” he said.

In April, the Biden Administration issued an intelligence report stating that China poses the biggest threat to the U.S. from its push for “global power.” The report warned that cyberattacks from China could disrupt and disable infrastructure and predicted that China would exert pressure on Taiwan to move toward unification, which will have significant implications for the electronics sector. Indeed, China has stated it wants to repatriate Taiwan.

Today, Taiwan accounts for about 60 percent of global semiconductor production. The vast majority of chip production in the country is by Taiwan Semiconductor Manufacturing Corporation (TSMC), accounting for about 60 percent of total chip production. Intel, the largest chip company globally, is reportedly making a massive investment in fab capacity for both leading-edge and trailing-edge chip technology.

Both TSMC and Korea’s Samsung Foundry have plans to build new fabs in the U.S. “Samsung and TSMC are best in class,” said Dale Ford, Research Director, ECIA. “We need them to be making these investments because the U.S. can’t do it alone.”

Samsung has filed papers in Arizona, New York and Texas outlining its plans for a leading-edge semiconductor manufacturing facility that would go online by the end of 2023. The Texas proposal would locate the fab near its existing operations in Austin, at an estimated cost is over $17 billion. Samsung hasn’t announced the technology it would be implementing.

TSMC is eyeing Arizona for an investment of $12 billion, most likely in a 5 nm fab. There is also speculation that the figure could be three times higher at $35 billion.

Both investments are being watched closely, especially the TSMC investment, because of China’s rhetoric about the repatriation of Taiwan. If this happens, the supply of semiconductors to the U.S. from TSMC and other Taiwanese chip makers would likely be impacted. Similarly, products and services from Taiwanese contract manufacturers such as Foxconn, Quanta and Compal may be affected as well. This could be catastrophic for virtually all major industries in the West.

- Climate change

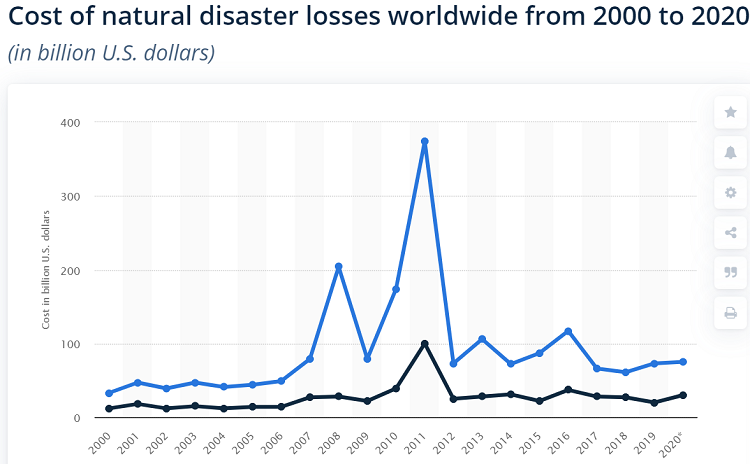

The number and severity of extreme weather events is increasing due to rising CO2 in the atmosphere and oceans. For instance, the number of hurricanes in the Atlantic in 2020 hit a record high of 31. It was the fifth costliest hurricane season since data was first collected in 1851.

A recent McKinsey report suggested companies can expect supply chain disruptions from extreme weather and other catastrophic events lasting a month or longer will occur every 3.7 years, with severe events taking a significant financial toll. That translates to about 45 percent of one year’s earnings could be lost each decade because of disruptions.

Source: Statistica

Similarly, a Jabil survey asked 715 OEM supply chain decision-makers which types of disruptions impacted their company’s supply chain in the last ten years. Seventy-eight percent said Covid-19, 50 percent said material shortages, 46 percent said geopolitics and trade instability, and 35 percent said natural disasters. The natural disaster category is likely to increase in the coming years due to climate-related natural disasters, which will severely disrupt supply chain operations and transportation.

2011 was the costliest year so far this century in terms of economic losses. Japan’s catastrophic tsunami and nuclear accident in March 2011 caused devastating destruction to infrastructure, plant closures and supply chain disruptions. A few months later, devastating monsoon flooding in Thailand closed factories that manufacture automotive parts, disk drives and other parts used to manufacture computers and digital products. The ripple effect of the floods shuttered manufacturing in Japan, China, the U.S. and many other countries.

The prospect of a warmer planet suggests an increase in the incidence and strength of severe weather events and supply chain disruptions, which requires a robust resilience plan for the entire supply chain.

- Cybersecurity

Cybersecurity is a priority for supply chain operations as cybercriminals become more sophisticated and companies migrate data processing and storage to the cloud. Covid-19 contributed to the rise in cyberattacks as office workers by the millions set up shop at home, often without adequate corporate security protection on their digital devices. One consequence was a dramatic 715 percent increase in ransomware attacks, according to ZDNet.

As the pace of digitization accelerates with the proliferation of IoT devices and the rollout of 5G, cybersecurity will undoubtedly become an even more critical issue for national security, business continuity, and the integrity of supply chain networks.

It is common practice for cybercriminals to target the weakest link in the supply chain as a way to gain access to more cyber-mature supply chain members, including tier-1 suppliers and OEMs, according to research conducted by the National Institute for Science and Technology (NIST). Identifying, assessing, and mitigating cyber supply chain risks is critical to ensure business continuity and resilience, requiring close collaboration with key suppliers.

- Random shocks

Unrelated to Covid-19, geopolitics, security, and climate change, there are random disasters waiting to happen. A recent example is the Ever Given incident in the Suez Canal in March 2021. The massive super-sized cargo ship got stuck in the Suez Canal for six days, costing billions in late shipments of goods from Asia to Europe and the Americas. While catastrophes like this are unpredictable, they need to be factored into the cost of managing global supply chains.

While impossible to predict or plan for, dealing with these random shocks needs to be factored into rapid-response planning to manage global supply chains.

Toward supply chain resilience

For at least the past 20 years, many companies have optimized supply chains to achieve efficiency, using year-over-year cost reduction as the metric for success. However, the Covid-19 pandemic, geopolitics and trade tensions, climate-related disasters and cybersecurity disruptions change the risk profile of global supply chains and how companies measure their performance.

Recent research suggests that flexible and resilient supply chains can deliver more than productivity improvement: they can generate new value and profitable growth in the long term.

Today’s supply chains were built to be just in time, not just in case. We live in a different environment today, where companies need to think strategically about resilience. They are experts in measuring and managing efficiency. The critical question now is how do they measure and manage resilience?

Additional articles in this report: