The decades old concept of creating multi-faceted corporate conglomerates in order to create size synergies seems to be fading, as large corporations with diverse operations are abandoning the concept. General Electric (GE), Toshiba (TOSBF), and Johnson & Johnson (JNJ) are among those that have recently announced break-ups.

One company bucking the trend is 3M (MMM), at least so far. With a diverse product range that includes such items as Post-It notes, medical tape, air filters, power tools, automotive parts, and lubricants, 3M has a long history of product innovation. As one would expect, the company serves many industries including Automotive, Consumer, Construction, Electronic, Energy, Safety and Transportation.

I am bullish on MMM, as supply chain issues will eventually fade and investors will turn away from risky money-losing tech stocks to focus on quality dividend payers.

See MMM Stock Charts on TipRanks>>>

Supply Chain Issues

If there’s any company that would be most materially affected by the 2021 supply chain disruptions, it is 3M. That’s because the company has manufacturing sites in 35 countries and works with over 300 suppliers.

These supply chain issues, as well as raw material price increases, reduced operating margins in the most recent quarter by 2.7%. This is despite mid-single digit organic revenue growth across most segments.

In order to deal with these problems, the company stated it is moving product using different formats, such as rail traffic, shipping from ports not showing congestion, and 40% more charter freight aircraft flights. Logistics and software infrastructure have also been upgraded to better track the flow of goods in real-time.

3rd Quarter Review

Sales growth remained strong, as global end-use demand has remained robust. The Consumer segment show the highest level of growth, with organic sales increasing 8.1%. That’s likely because stimulus-driven spending and pandemic recovery purchases are still driving consumer activity.

Next was Safety & Industrial, which grew 6.1%. Pockets of strong industrial growth were in the areas of adhesives, tapes, and abrasives. Transportation & Electronics grew 5.8% and was led by advanced materials and transportation safety. Organic sales declined in Electronics due to the continued impact of semiconductor shortages with customers.

Lastly, Healthcare grew 4.1% and was led by food safety, oral care, and healthcare information systems. Higher levels of growth in this segment were offset by declines in disposable respirator sales after facing tough comps from the 2020 pandemic year.

EPS growth was flat, due to the supply chain constraints effects on operating margins. Raw material price increases also negatively affected operating margins.

3M typically generates strong levels of free cash flow and was able to return $1.4 billion in cash to shareholders. This was comprised of $856 million in dividend payments and $527 million in gross share repurchases.

Macro Trends

As a global conglomerate, 3M usually has its pulse on macro-economic and business trends around the world. The company stated that end-market demand remains strong around the world as the post-pandemic recovery continues to take hold. However, the global semi-conductor shortage remains an issue for many of 3M’s customers, which subsequently affects 3M’s sale of certain electronic and industrial products to these customers.

3M also has a good sized exposure to the healthcare and dental markets in terms of elective procedures, and the company indicated trends remained stable. The company did not forecast an end to the supply chain issues but stated “significant global supply chain, raw materials and logistics challenges are expected to persist into foreseeable future.”

Valuation and Dividend

MMM stock has retreated from its 2021 highs of $206 down to around $179 today. EPS estimates for 2021 are $9.87 and $10.43 for 2022. A 17x forward P/E does not seem unreasonable, as those numbers take in account supply chain disruptions and raw material inflation. Normalized earnings would likely produce a P/E in the mid-teens range.

3M’s dividend yield is well above market averages, at 3.23%. The $5.92 yearly dividend produces a relatively high 60% payout ratio on 2021 estimates of $9.87. However, as noted above, 2021 and 2022 are not reflective of the company’s full earnings potential.

I am bullish on MMM stock as the valuation is not stretched like so many companies today in this never-ending bull market. In addition, based on its 120-year history, the company will continue to innovate and survive whatever economic environment or business challenges come its way.

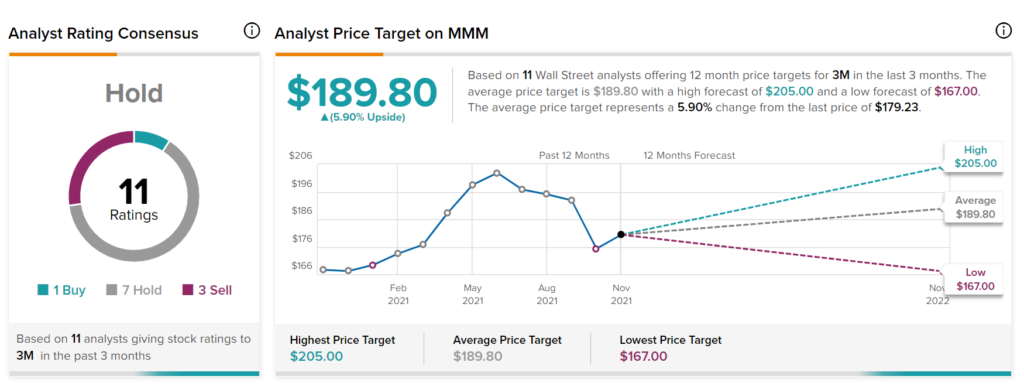

Wall Street’s Take

Turning to Wall Street, MMM has a Hold consensus rating based on 1 Buy, 7 Hold, and 3 Sell ratings assigned in the past three months. At $189.80, the average MMM price target implies 5.90% upside potential.

Disclosure: Disclosure: At the time of publication, Tom Kerr did not own shares of any stocks mentioned above.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates, and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices or performance.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.